Car insurance can feel expensive when it lands on top of fuel, maintenance, rent, groceries, and everything else. That is why many drivers look for payment flexibility. But the real question is not only whether you can split the cost. It is whether the payment structure fits your budget without creating bigger problems later. In many cases, Buy Now Pay Later car insurance is best understood as a payment arrangement layered onto a standard auto policy, not a completely separate type of coverage.[1]

If you are new to the concept, start with what buy now pay later car insurance is. Then compare it with other BNPL car insurance options so you can judge the structure, the fees, and the long-term fit more clearly.

When it can help

BNPL can reduce the amount due upfront and make coverage easier to start.

What to compare

Total cost, payment rules, coverage quality, and what happens if you miss a payment.

Main risk

A low first payment can hide fees, tighter terms, or a higher total cost.

Best fit

Drivers who need lower upfront pressure and can reliably manage recurring payments.

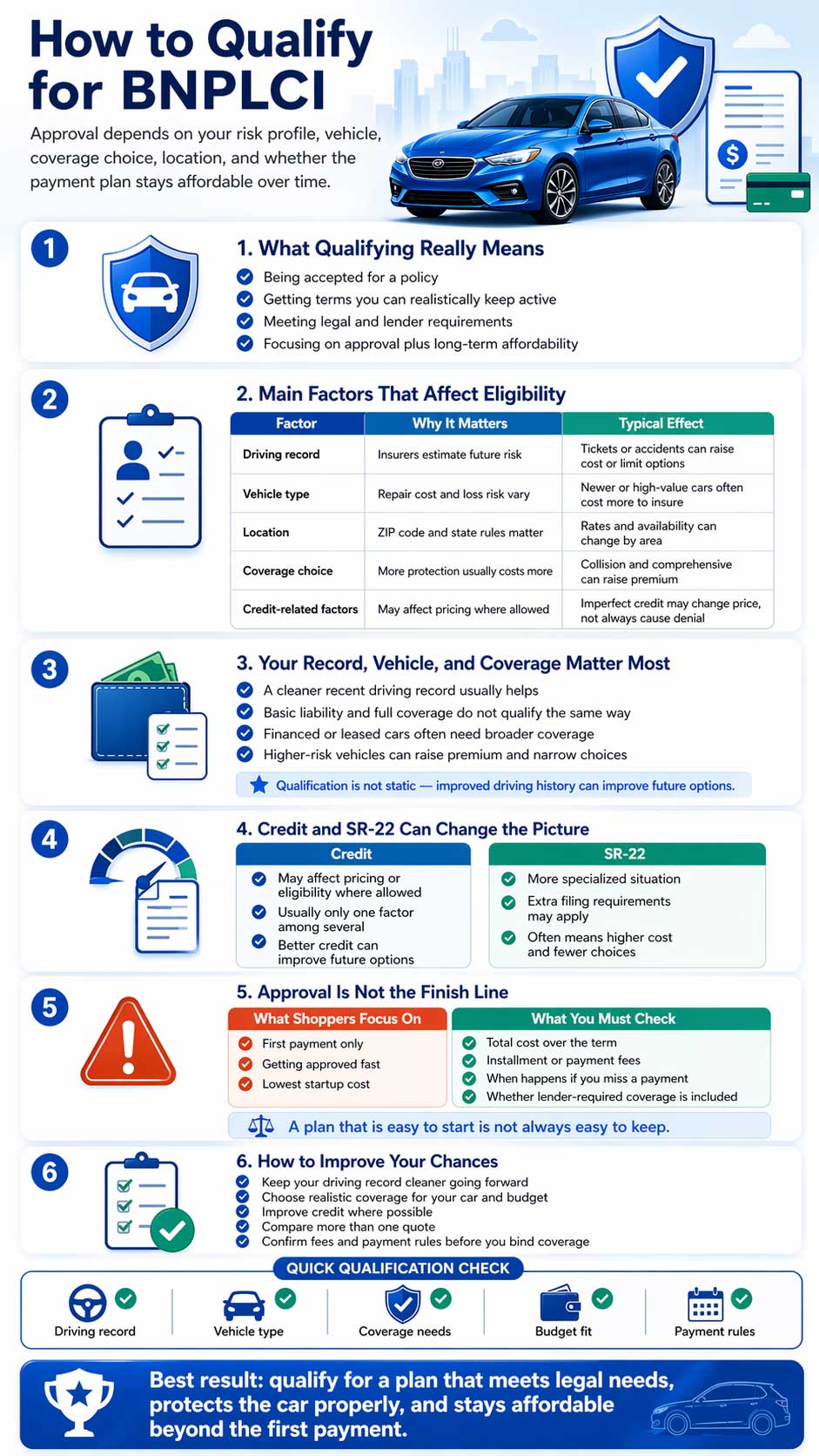

What BNPL Car Insurance Usually Means

Buy Now Pay Later car insurance usually refers to a payment arrangement where the premium is split into installments rather than paid in one larger amount at the beginning. California’s DFPI explains that premium finance companies may advance money directly or indirectly to an insurer or producer at the insured’s request under a premium finance agreement.[1] In simple terms, the coverage may still look similar to a traditional policy, but the billing setup is structured to spread the cost over time.

That can be useful when upfront cost is the biggest obstacle. But a lower starting payment should never be confused with guaranteed savings. A plan that feels easier today can still cost more by the end of the term if service fees, installment charges, or payment-related penalties apply.

When BNPL Can Be a Good Fit

BNPL-style payments may be a good fit when your main challenge is the size of the first payment. This can matter if you need coverage quickly and do not want one large bill to disrupt your monthly essentials. For some drivers, the ability to spread payments out can make it easier to start or maintain coverage instead of going uninsured because the initial price feels out of reach.

- You need a lower amount due at the start of coverage.

- You have steady enough cash flow to handle scheduled payments reliably.

- You understand the total amount you will pay over the term.

- You are using flexible payments to manage cash flow, not to ignore the true cost.

If your main goal is reducing the initial burden without losing sight of value, it may also help to review affordable coverage without a down payment.

When BNPL Might Not Be Right for You

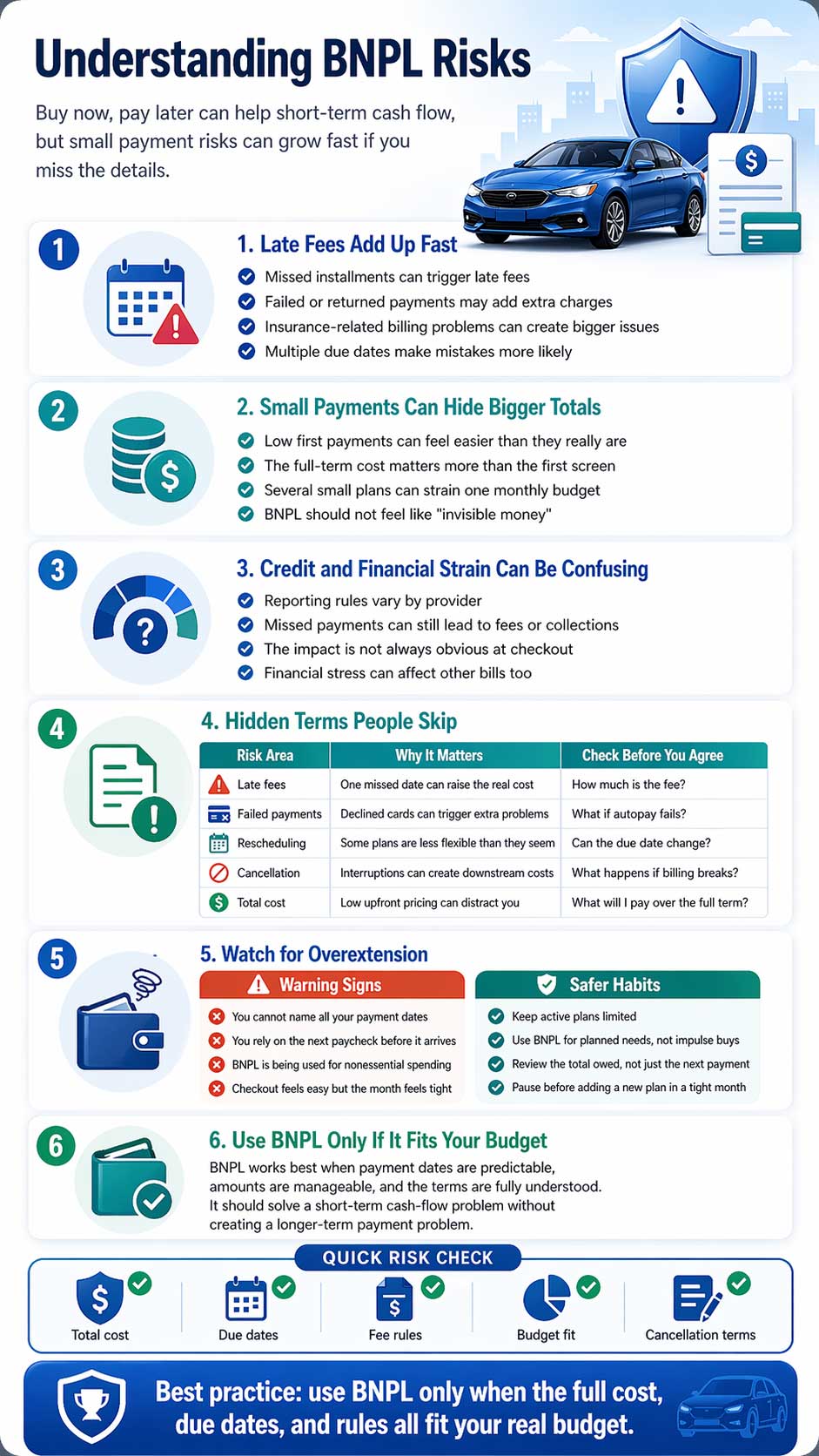

BNPL is not always the right answer. It can look cheaper at signup while becoming more expensive later if fees stack up or if the recurring payment schedule is harder to maintain than expected. California’s Department of Insurance notes that insurers may have fee categories tied to billing and policy administration, including installment fees, late fees, cancellation fees, reinstatement fees, premium finance revenues, and installment finance charges.[2]

Practical takeaway: the best question is not “How low is the first payment?” It is “What is the full amount I will pay by the end of the policy term, and what happens if I fall behind?”

Fees can add up

A smaller upfront payment may still lead to a higher total bill.

Missed payments matter

Late or missed payments can trigger penalties, cancellation, or reinstatement issues.

Some plans are stricter

Not every provider offers the same flexibility, grace periods, or coverage options.

Budget stress can show up later

A plan that feels easy on day one may feel different after several recurring payments.

That is why it is smart to compare terms closely and also review the main BNPL risks before you commit.

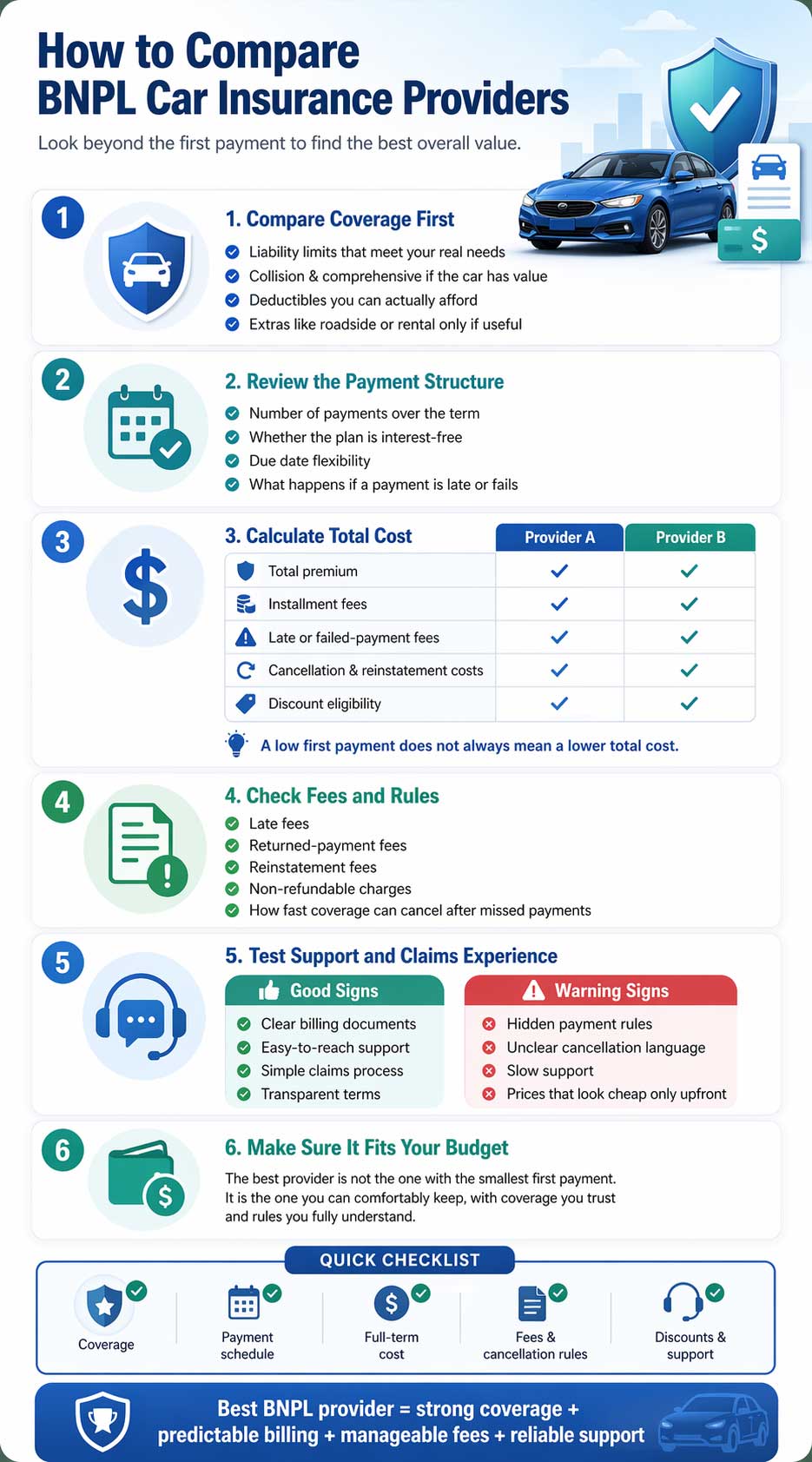

Coverage Still Has To Make Sense

Payment flexibility is only one part of the decision. You still need the right protection. Washington’s insurance guidance explains that collision covers damage to your car from a crash, while comprehensive covers losses such as theft, vandalism, fire, hail, or other non-collision events.[3] That means a lower starting payment is not a win if the quote leaves you underinsured or strips out protection you actually need.

| What to Compare | Why It Matters |

|---|---|

| Liability limits | You still need limits that fit your legal obligations and real risk. |

| Collision and comprehensive | These can matter a lot on financed, leased, or newer vehicles. |

| Deductibles | A lower premium can come with a deductible that is harder to absorb after a loss. |

| Optional add-ons | Roadside assistance, rental reimbursement, and other extras can change the policy’s value. |

Will BNPL Work With Your Financial Habits?

This may be the most important question of all. BNPL-style insurance can be useful for drivers who stay organized with due dates and want lower upfront friction. It may be less suitable for someone who already struggles with recurring payments or wants to minimize monthly obligations. The strongest plans are the ones you can keep stable, not just the ones you can start.

- Cash flow: Do you need a lower upfront amount right now?

- Consistency: Can you make every payment on time without stress?

- Total cost: Have you checked the full amount paid across the term?

- Coverage: Are you still keeping the protections you actually need?

- Rules: Do you understand late fees, cancellation, and reinstatement terms?

Financed Vehicles Make the Decision More Serious

If your vehicle is financed or leased, the stakes are higher. The CFPB explains that if your insurance lapses, the lender can obtain force-placed insurance to cover the vehicle. That coverage protects the lender and vehicle, but not you.[4] So if you are choosing BNPL only because the first payment is smaller, make sure the later payments are still realistic. A lapse can become much more expensive than the initial problem you were trying to solve.

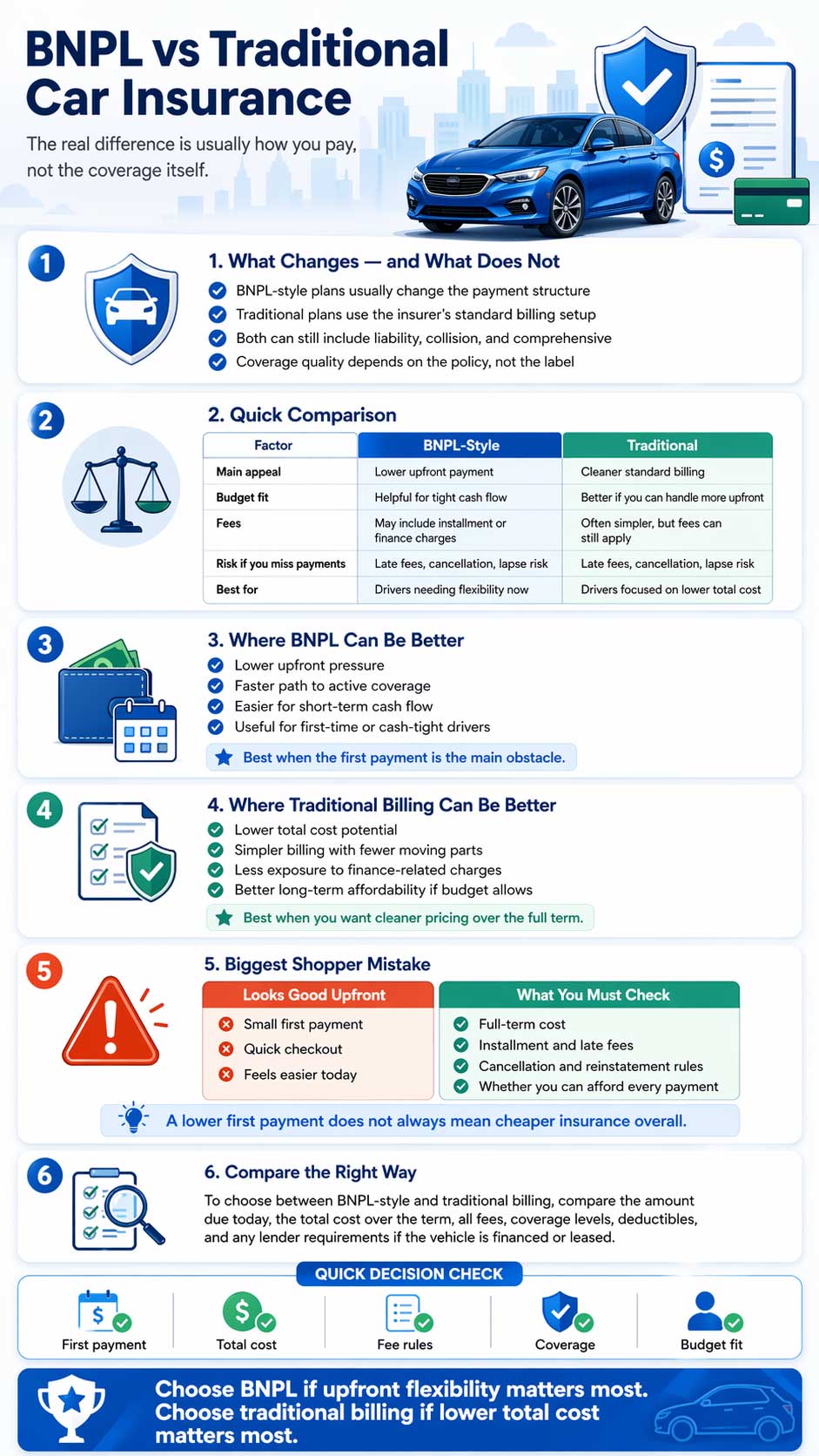

| Category | BNPL-Style Payments | Traditional Billing |

|---|---|---|

| Upfront cost | Often lower | Often higher |

| Fees to review | Installment, service, late, or finance-related charges | Possible billing, late, cancellation, or reinstatement fees |

| Total cost | Can rise if fees add up | Can be lower overall if fewer add-on charges apply |

| Best fit | Drivers who need lower upfront pressure and can manage recurring payments | Drivers who can handle a larger first payment and want a simpler structure |

FAQ

What is Buy Now Pay Later car insurance?

In most cases, it means paying for a standard auto policy through installments or a premium-finance-style arrangement instead of making one larger upfront payment.

Are there fees associated with BNPL insurance?

Yes, there can be. Depending on the arrangement, you may see installment fees, late fees, cancellation charges, reinstatement costs, or other payment-related charges.

Who benefits most from BNPL insurance?

Drivers who need a lower upfront cost and can reliably handle scheduled payments often benefit the most, especially when they compare total cost carefully first.

What is the biggest mistake to avoid?

The biggest mistake is focusing only on the first payment. You should always compare the total cost, the fee structure, and the coverage you are keeping.

Final Thoughts

BNPL car insurance can be a smart option when upfront cost is the biggest obstacle. But it is only the right fit if the fees are transparent, the total price still makes sense, and you are confident you can stay on schedule. A flexible payment model can help with budgeting, but the best choice is still the one that gives you the right protection at a cost you can realistically maintain.

Compare more than the first payment

Before choosing any plan, compare the full cost, the payment rules, and the coverage details side by side. Visit BNPLCI to explore flexible options with more clarity.

References

- California Department of Financial Protection and Innovation — Insurance Premium Finance↩

- California Department of Financial Protection and Innovation — Premium Finance Agreements and Licensed Activity↩

- California Department of Insurance — Prior Approval Rate Filing Instructions↩

- Washington Office of the Insurance Commissioner — A Consumer’s Guide to Auto Insurance↩

- Consumer Financial Protection Bureau — What Kind of Auto Insurance Options Are Available When Financing a Car?↩