By

BNPLCI.com Editorial Team

— Insurance content contributors

Editorially reviewed informational content about U.S. car insurance payment options, low upfront payment structures, flexible billing, and BNPL-style insurance shopping.

Created on October 15, 2025 · Last updated on June 24, 2026

Flexible payment options guide

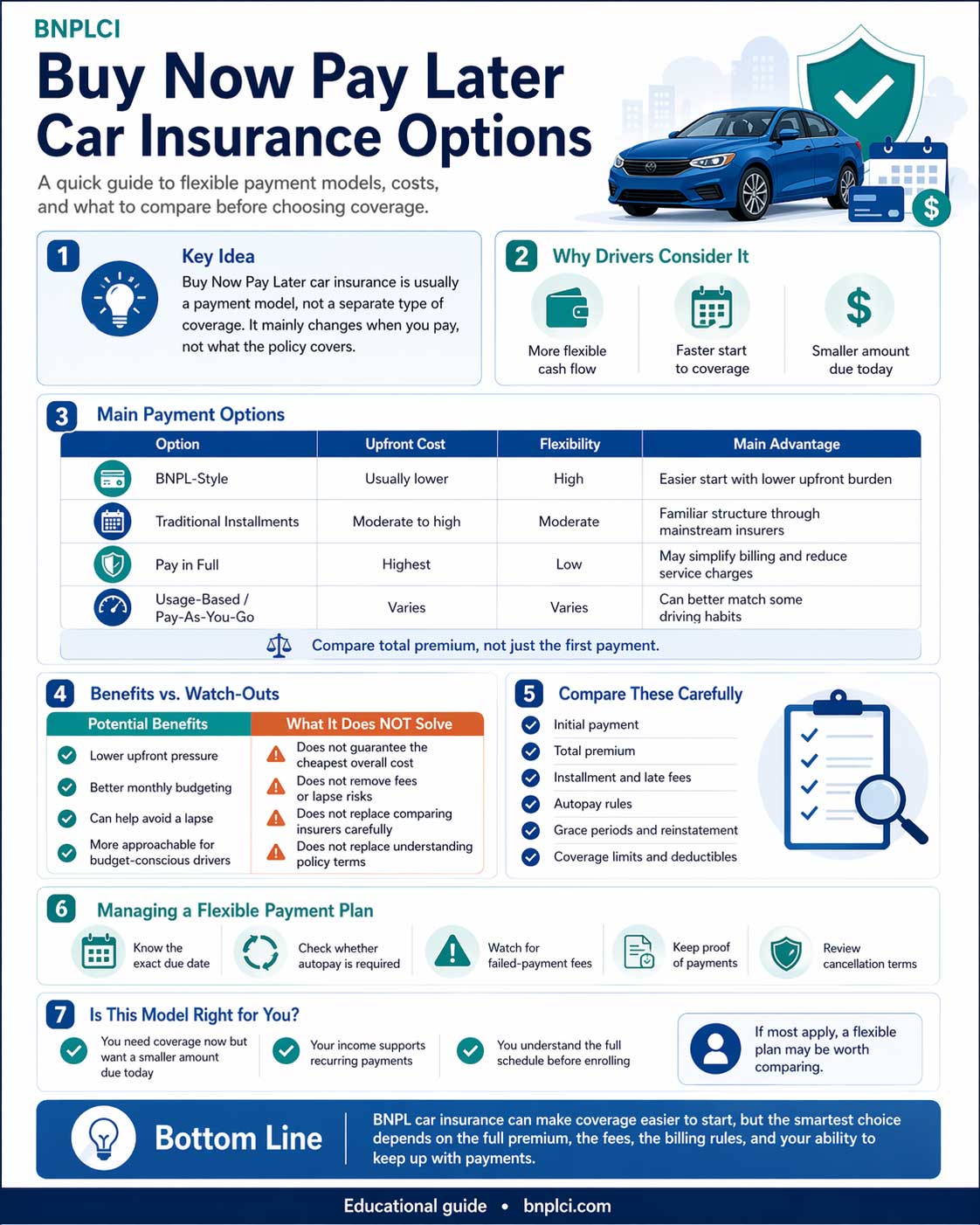

Buy Now Pay Later car insurance options are best compared by looking at the full payment structure, not just the first amount due. Some drivers want a lower first payment, others want predictable monthly installments, and others may prefer usage-based or pay-in-full alternatives if those options lower the total cost.

This guide compares the main BNPL-style and flexible auto insurance payment options side by side, including low first-payment policies, monthly installment plans, no-down-payment advertised plans, usage-based models, autopay billing options, and pay-in-full alternatives.

The goal is not simply to find the smallest upfront number. The better approach is to compare coverage limits, deductibles, fees, cancellation rules, total premium, and payment due dates before starting a policy.[1][2]

Compare Payment Types

Look beyond one advertised payment and compare how each option handles deposits, installments, service fees, and renewal billing.

Check the Total Cost

A lower first payment may help today, but the full policy cost can still be higher if fees or less favorable terms apply.

Match Your Budget

The best option is the one you can keep active without missing payments, risking a lapse, or reducing coverage too much.

Buy Now Pay Later Car Insurance Options Compared

The phrase “Buy Now Pay Later car insurance” is often used broadly. If you need the basic definition first, BNPLCI also explains what Buy Now Pay Later car insurance means. In practice, drivers may be comparing several different payment structures. Some are traditional auto insurance billing options with a lower amount due upfront. Others are installment arrangements, agency billing options, usage-based policies, or alternatives that reduce the total cost in a different way.

The table below separates the main options so you can see what each one usually changes, who it may help, and what to review before choosing.

| Option |

How It Usually Works |

Best For |

Main Advantage |

Main Watch-Out |

| Low First-Payment Car Insurance |

You start coverage with a smaller initial payment, then continue with scheduled payments. |

Drivers who need coverage now but cannot comfortably pay a large amount upfront. |

Can make starting a policy more manageable. |

The total policy cost may still be higher than a pay-in-full option. |

| Monthly Installment Auto Insurance |

The premium is divided into monthly payments over the policy term. |

Drivers who prefer predictable recurring billing. |

Easier to fit into a monthly budget. |

Installment or service fees may apply. |

| No-Down-Payment Advertised Plans |

Marketing may emphasize very low upfront cost, but some amount may still be due to activate coverage. |

Drivers searching for the lowest realistic amount due today. |

Can reduce the first payment barrier. |

“No down payment” does not always mean zero dollars due. |

| Agency or Broker Payment Arrangements |

An agency, broker, or payment partner may help place coverage with a carrier and arrange billing terms. |

Drivers who want help comparing multiple providers or payment structures. |

May give access to more than one carrier or billing setup. |

Always review fees, cancellation terms, and who actually provides the insurance. |

| Usage-Based or Pay-Per-Mile Insurance |

Pricing may depend partly on mileage, driving behavior, or telematics data. |

Low-mileage drivers or drivers comfortable with tracking-based programs. |

May lower costs for some drivers with limited driving. |

Pricing can vary based on driving patterns and program rules. |

| Autopay or Electronic Billing Options |

You set up automatic payments or paperless billing, sometimes with a billing discount depending on the insurer. |

Drivers who are organized and want fewer missed-payment risks. |

Can simplify payment management. |

A failed payment can still create fees or cancellation risk. |

| Pay-in-Full Alternative |

You pay the full policy premium upfront for the term. |

Drivers with enough cash available who want simpler billing. |

May avoid installment fees and reduce payment stress later. |

Requires the largest upfront payment. |

Quick takeaway: the best BNPL-style car insurance option is not always the one with the lowest first payment. It is the option that gives you enough coverage, a manageable payment schedule, and the lowest realistic total cost for your situation.

Which Option Fits Each Driver Situation?

A useful way to compare Buy Now Pay Later car insurance options is to start with the driver’s real problem. Some shoppers need the lowest amount due today, while others need lower total cost, fewer billing surprises, or a payment schedule that lines up with their paycheck. The same option will not be best for every driver.

| Driver Situation |

Option to Compare First |

Why It May Fit |

Extra Check Before Buying |

| You need coverage active today |

Low first-payment policy or monthly installment plan |

These options may reduce the first-payment barrier while still starting a standard auto policy. |

Confirm the exact amount due before coverage begins and keep proof of payment. |

| You drive very few miles |

Usage-based or pay-per-mile insurance |

Some low-mileage drivers may save more by lowering the premium itself instead of only spreading payments out. |

Check mileage rules, telematics requirements, and how rates can change after enrollment. |

| You want fewer surprise fees |

Pay-in-full or low-fee installment billing |

Paying in full may avoid some billing charges, while a transparent installment plan can make recurring costs easier to plan. |

Compare the total term cost, not only the monthly number shown in the quote. |

| Your income arrives on fixed dates |

Autopay or scheduled monthly billing |

A predictable draft date can help avoid missed payments when it is matched to your income cycle. |

Make sure the payment date is realistic and that failed-payment rules are clear. |

| You are choosing between several carriers |

Agency, broker, or comparison-based shopping |

Comparing carriers can show whether another company offers a more manageable first payment or better total cost. |

Verify who issues the policy, what fees apply, and whether the quote includes the coverage you actually need. |

Option 1: Low First-Payment Car Insurance

Low first-payment car insurance is often the closest match for drivers searching for Buy Now Pay Later car insurance options. The idea is simple: instead of paying a large amount before coverage starts, you pay a smaller first amount and then continue with scheduled payments.

This option may help if you need proof of insurance quickly, are switching providers, or are trying to avoid a lapse. However, the first payment should never be judged alone. Ask whether the lower upfront amount creates higher monthly payments, installment fees, or stricter cancellation rules later.

- Ask how much is due today to activate coverage.

- Compare the total six-month or twelve-month policy cost.

- Check whether installment fees are added to each payment.

- Confirm how quickly coverage could cancel after a missed payment.

Option 2: Monthly Installment Auto Insurance

Monthly installment billing is one of the most common flexible payment options. Instead of paying the whole premium upfront, the driver pays on a schedule. This can make insurance easier to budget because the cost becomes part of a monthly routine.

The tradeoff is that monthly billing can include service charges or installment fees depending on the insurer and state. The monthly payment may look manageable, but the total amount paid over the policy term may be higher than a pay-in-full policy.

When Monthly Installments May Help

- You prefer predictable monthly bills.

- You do not want one large insurance payment.

- Your income arrives on a regular schedule.

- You can keep track of payment due dates.

What to Check First

- Monthly service charges.

- Autopay requirements.

- Late-payment fees.

- Cancellation and reinstatement rules.

Option 3: No-Down-Payment Advertised Plans

Some drivers search for no-down-payment car insurance because they want to start coverage with as little money as possible. The important point is that “no down payment” is often used as a marketing phrase. In many cases, a first payment may still be required to activate the policy.

That does not mean the option is useless. It can still be helpful if the first required payment is lower than a traditional deposit. The key is to ask what the phrase means in the actual quote: zero dollars due, a reduced first payment, or simply the first month’s premium due at signup.

Important: do not assume a “no down payment” quote means free coverage today. Auto insurance generally requires payment before or when coverage begins, and terms vary by insurer, state, driver profile, and billing structure.

Option 4: Agency or Broker Payment Arrangements

Some drivers work with agencies, brokers, or comparison services to find a carrier and payment plan that fits their budget. If you are comparing several companies, it can also help to review how to compare BNPL car insurance providers. This can be useful when one insurer’s first payment is too high but another insurer offers a more manageable billing structure.

The main advantage is comparison. Instead of assuming one quote is the only option, you may be able to review multiple carriers, policy terms, and payment schedules. The main watch-out is transparency: you should know who the insurer is, what fees apply, how cancellation works, and whether any third-party payment terms are involved.

- Ask which insurance company will issue the policy.

- Ask whether the agency charges separate fees.

- Confirm whether the payment plan is with the insurer or another party.

- Request the full payment schedule before agreeing.

Option 5: Usage-Based or Pay-Per-Mile Insurance

Usage-based insurance and pay-per-mile insurance are not the same thing as BNPL, but they can be relevant alternatives for drivers trying to lower insurance costs. Instead of focusing only on payment timing, these programs may adjust pricing based on mileage, driving behavior, or telematics data.

This option may make sense for people who drive less than average, work from home, use public transportation often, or have access to another vehicle. It may be less attractive for drivers who commute long distances or are uncomfortable with tracking-based programs.

Potential Benefits

- May reduce cost for low-mileage drivers.

- Can match pricing more closely to driving habits.

- May provide feedback on driving behavior.

Potential Concerns

- Not ideal for high-mileage drivers.

- Program rules vary widely.

- Some drivers may not want telematics tracking.

Option 6: Autopay and Electronic Billing Options

Autopay and electronic billing do not always change the premium dramatically, but they can make a flexible payment plan easier to manage. Some insurers may offer billing-related savings, while others mainly use autopay to reduce missed-payment risk.

This option works best for drivers who keep enough money in their account before each due date. It can be risky if your balance changes often or if a failed payment could trigger fees, returned-payment charges, or cancellation notices.

- Confirm the exact draft date.

- Ask whether autopay changes your billing fees.

- Keep payment confirmation records.

- Update the payment method before a card expires.

Option 7: Pay-in-Full as the Alternative

Pay-in-full is not a BNPL option, but it belongs in the comparison because it can sometimes be the cheaper route overall. If you can afford the upfront cost, paying in full may reduce billing complexity and may help avoid installment charges.

The downside is obvious: it requires more money at the beginning. For many drivers, that is exactly why BNPL-style options are attractive. Still, comparing pay-in-full against flexible billing gives you a clearer view of the true price difference.

How to Choose the Right BNPL-Style Car Insurance Option

Choosing the right option starts with separating affordability today from affordability over the full policy term. A low first payment may solve an immediate problem, but the plan only works if the later payments fit your budget too.

The NAIC recommends comparing coverage, deductibles, limits, and insurer information when shopping for auto insurance. That same logic applies when comparing payment options: the billing schedule matters, but it should not replace a careful review of the policy itself.[3]

| Question |

Why It Matters |

What to Look For |

| How much is due today? |

This determines whether you can actually start coverage now. |

Initial payment, fees, taxes, and required first installment. |

| What is the total policy cost? |

A low first payment can hide a higher total cost. |

Total premium, installment charges, and service fees. |

| What happens if I miss a payment? |

Missed payments can lead to fees, cancellation, or a coverage lapse. |

Grace period, late fees, reinstatement rules, and cancellation timing. |

| Are my coverage limits enough? |

Cheap payment plans are not helpful if coverage is too weak. |

Liability limits, deductibles, comprehensive, collision, and state requirements. |

| Is the insurer reliable? |

Billing flexibility does not replace claims service and policy support. |

Company reputation, complaint information, and customer service access. |

Where These Options Fit in Your Insurance Search

If your main problem is the amount due today, start by comparing low first-payment policies and monthly installment options. If your main problem is the total premium, compare discounts, coverage choices, usage-based programs, and pay-in-full pricing. If your main problem is payment timing, ask about autopay, billing dates, and whether the insurer can align payments with your income schedule.

BNPL-style insurance shopping is useful when it helps you keep coverage active without overextending your budget. It is also worth reviewing the main BNPL risks before choosing a plan. It becomes risky when the lower first payment causes you to ignore fees, weak coverage, or a payment schedule you cannot maintain.

Helpful BNPLCI Guides to Compare Next

After reviewing the main options above, these BNPLCI guides can help you compare payment terms, provider choices, risks, and fee questions more carefully:

Common Mistakes That Can Keep a Flexible Plan From Being Worth It

A flexible payment plan can be helpful, but it can also create problems if the shopper focuses only on the first payment. Before choosing a BNPL-style car insurance option, look for mistakes that can make the policy harder to keep active.

- Comparing only the first payment: a lower amount due today may come with higher later payments or billing fees.

- Reducing coverage too far: a cheaper payment is not useful if liability limits, deductibles, or optional coverages no longer fit your risk.

- Ignoring cancellation rules: a missed installment can lead to a lapse, reinstatement issue, or proof-of-insurance problem.

- Assuming every “no down payment” quote means zero dollars: many offers still require a first payment before coverage starts.

- Not saving documents: keep the quote, declarations page, billing schedule, payment confirmations, and cancellation notices in one place.

Credit, Fees, and Payment Management

Payment terms can vary depending on the provider and how the arrangement is structured. Consumer BNPL products can differ in fees, repayment timing, credit reporting practices, and dispute handling, which is why the CFPB has studied BNPL market trends and consumer impacts.[4]

Auto insurance billing is not always the same as retail BNPL financing, so you should read the specific policy and billing documents before assuming how payments, fees, or reporting work. BNPLCI also has separate guides on hidden BNPL car insurance fees and how BNPL may affect your credit score. If a third-party payment arrangement is involved, ask whether missed payments can create separate financial consequences beyond the insurance policy itself.

- Read the billing agreement before starting coverage.

- Ask whether installment fees apply.

- Check whether failed payments create extra charges.

- Confirm cancellation timing after a missed payment.

- Keep records of payment confirmations and policy documents.

FAQ

What are the main Buy Now Pay Later car insurance options?

The main options include low first-payment policies, monthly installment plans, no-down-payment advertised plans, agency or broker billing arrangements, usage-based insurance, autopay billing, and pay-in-full alternatives.

Is Buy Now Pay Later car insurance a separate type of coverage?

Usually, no. It is more often a way to describe a payment structure. The actual coverage still needs to be reviewed like any other auto policy, including liability limits, deductibles, exclusions, and optional coverages.

Does no-down-payment car insurance mean zero dollars today?

Not always. In many cases, a first payment may still be required to activate coverage. The phrase may mean a reduced upfront payment rather than truly free coverage at the start.

Which option is best if I need coverage immediately?

A low first-payment policy or monthly installment plan may be helpful if you need coverage quickly. Still, you should compare the total cost, payment schedule, cancellation rules, and coverage limits before choosing.

Can BNPL-style car insurance cost more overall?

Yes. A lower first payment can be useful, but the total cost may be higher if installment fees, service charges, or less favorable policy terms apply.

Should I choose the lowest first payment available?

Not automatically. The lowest first payment may not be the best deal if the monthly payments are too high, the coverage is too limited, or the policy includes fees that raise the total cost.

What should I compare before choosing a flexible payment option?

Compare the first amount due, the total policy cost, installment fees, billing dates, cancellation rules, deductibles, liability limits, and whether the insurer or agency clearly explains who issues the policy.

Conclusion

Buy Now Pay Later car insurance options are most useful when they help you start or maintain coverage without creating a payment schedule you cannot handle. The strongest options are not always the ones with the smallest first payment. They are the ones that balance upfront affordability, total premium, coverage quality, billing rules, and realistic monthly costs.

Before choosing a plan, compare low first-payment policies, monthly installments, no-down-payment advertised plans, usage-based alternatives, autopay options, and pay-in-full pricing. A flexible payment structure can help, but the real goal is to keep reliable coverage active at a cost you can manage.