Affordable no-down-payment car insurance is not just about finding the smallest first payment. A truly useful policy should lower the amount due at the start while still giving you enough coverage, clear billing terms, and a total cost you can manage over the full policy period.

Many drivers compare low-upfront quotes because they need coverage quickly, want to avoid a lapse, or cannot comfortably pay a larger opening bill. That can be a smart reason to shop. The risk is choosing a policy that looks affordable today but becomes expensive later because of weak limits, high deductibles, installment fees, or strict cancellation rules.

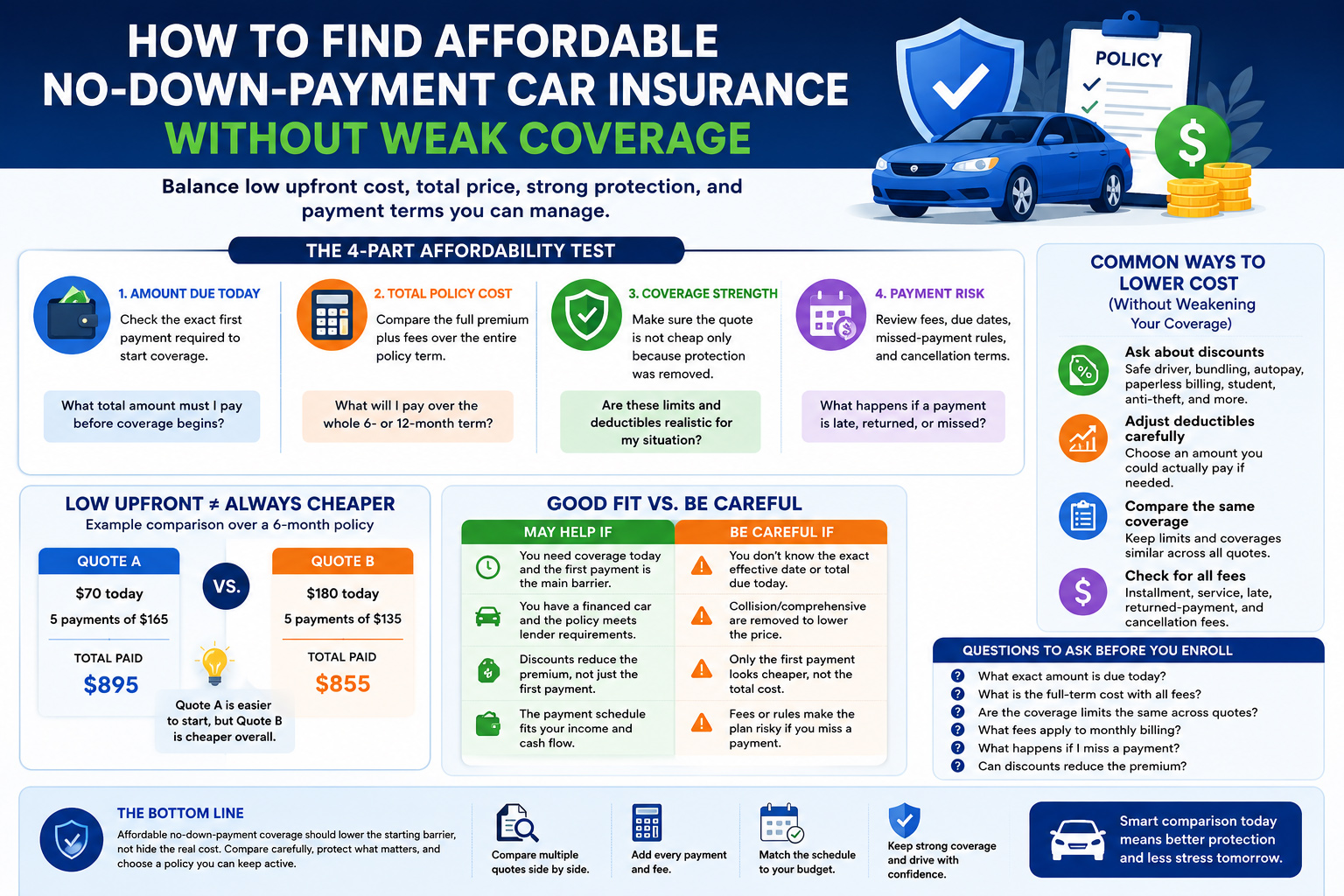

This guide shows how to find affordable coverage without weakening your protection. Use the four-part affordability test below before choosing any low-upfront policy.

Amount Due Today

Check the exact first payment needed before coverage becomes active.

Total Policy Cost

Compare the full-term premium, not only the first number shown in the quote.

Coverage Strength

Make sure the quote is not cheap only because key protection was removed.

Payment Risk

Review fees, due dates, missed-payment rules, and cancellation timing.

What Affordable No-Down-Payment Coverage Really Means

Affordable coverage without a down payment usually means a policy with a lower amount due at the beginning, not a policy that starts with no payment at all. In most cases, you should expect to make some form of first payment before coverage becomes active. The important question is whether that first payment is reasonable and whether the rest of the policy still works for your budget.

This page is different from a basic explanation of no-down-payment car insurance. Here, the focus is on how to compare affordability without sacrificing useful protection. For a broader look at billing choices, you can also review car insurance payment options and no-deposit insurance.

The 4-Part Affordability Test

Before choosing a low-upfront policy, compare the quote using four separate tests. A policy can pass one test and fail another. For example, it may be easy to start today but too expensive to keep active later.

| Affordability Test | What It Measures | Why It Matters | Question to Ask |

|---|---|---|---|

| Amount due today | The exact payment required to start coverage. | This determines whether the policy is realistic right now. | What total amount must I pay before coverage begins? |

| Total policy cost | The full premium plus fees across the policy term. | A small first payment can still lead to a higher total price. | What will I pay over the entire six- or twelve-month term? |

| Coverage strength | Liability limits, deductibles, optional coverage, and lender requirements. | A cheap quote may be cheap because it protects you less. | Are these limits and deductibles realistic for my situation? |

| Payment risk | Installment fees, late fees, cancellation rules, and failed-payment terms. | One missed payment can create extra cost or a lapse. | What happens if a payment is late, returned, or missed? |

When This Option May Help vs. When to Be Careful

Low-upfront coverage can be useful, but it is not the right choice for every driver. The table below helps separate situations where this type of policy may solve a real problem from situations where the low first payment may hide a weaker deal.

| Driver Situation | Affordable Option May Help If | Be Careful If | Better Comparison |

|---|---|---|---|

| You need coverage today | The first payment is the main barrier to starting a policy. | You do not know the exact effective date or total due today. | Compare startup cost and confirmed coverage timing. |

| You have a financed car | The policy meets lender requirements and still lowers upfront pressure. | Collision or comprehensive coverage was removed to lower the price. | Compare lender-required coverage, deductibles, and monthly payments. |

| You want a cheaper quote | Discounts reduce the actual premium. | Only the first payment is lower, but the full-term cost is higher. | Compare total premium after all discounts and fees. |

| You have tight cash flow | The payment schedule fits your paycheck and other bills. | Installment fees or late-payment rules make the plan fragile. | Compare monthly affordability and cancellation risk. |

| You are switching insurers | The new quote is better and the first payment is manageable. | You create a coverage gap or overlap the old and new policies unnecessarily. | Compare cancellation date, new effective date, refund timing, and fees. |

Example: Low Upfront Does Not Always Mean Cheaper

Imagine Quote A requires $70 today and then five monthly payments of $165. The total paid would be $895. Quote B requires $180 today and then five monthly payments of $135. The total paid would be $855.

Quote A is easier to start, but Quote B is cheaper over the term. That does not mean Quote A is always wrong. If you cannot afford $180 today, the lower first payment may solve a real cash-flow problem. But the decision should be made with the total cost in front of you, not only the startup amount.

1. Compare the Same Coverage First

The easiest way to make a quote look affordable is to reduce coverage. That can lower the first payment and the monthly premium, but it may also leave you underprotected. A fair comparison uses similar liability limits, similar deductibles, and similar optional coverages across each quote.

Auto insurance can include liability, property, and medical-related protections depending on the policy and state. Most states require auto liability insurance, but minimum limits may not be enough for every driver or vehicle.[1]

Coverage to Review

- State-required liability limits.

- Collision coverage if your vehicle needs physical damage protection.

- Comprehensive coverage for theft, weather, fire, or other non-collision losses.

- Uninsured or underinsured motorist options where available.

- Lender or lease requirements if the vehicle is financed.

Warning Signs

- The quote is cheap only because coverage limits are very low.

- Important coverages are removed without explanation.

- The deductible is higher than you could realistically pay.

- The quote hides exclusions, billing fees, or cancellation terms.

- The first payment is emphasized more than the policy details.

2. Compare the First Payment and the Full-Term Cost

A smaller first payment can be useful when money is tight, but it should never be the only number you compare. Ask every provider for the exact amount due today, the scheduled payment amount, the total premium, and any fees that apply during the policy term.

NAIC consumer shopping materials encourage drivers to compare policy details and ask about payment options, including whether monthly or quarterly payments add an extra charge.[2] That question is especially important when the policy is marketed around low upfront cost.

- Ask for the exact amount due before coverage begins.

- Ask for the full premium over the policy term.

- Ask whether monthly billing adds an extra charge.

- Ask whether paying in full would lower the total cost.

- Ask what happens if a payment is late, returned, or missed.

3. Use Discounts Before Cutting Protection

Discounts can make a policy more affordable without simply weakening coverage. Availability varies by insurer and state, but common categories may include safe driving, bundling, paperless billing, autopay, driver training, student eligibility, anti-theft features, or prior insurance history.

This is what separates a real affordability improvement from a risky low-price quote. A discount lowers the premium itself. Cutting coverage may only make the policy look cheaper while leaving you with more financial risk after a claim. For a discount-specific guide, review affordable no-down-payment car insurance discounts.

| Possible Discount Area | What to Ask | Why It Helps |

|---|---|---|

| Safe driver or claims-free history | Do recent clean driving years help my quote? | May reduce the premium without reducing protection. |

| Autopay or paperless billing | Does this lower cost or remove a billing fee? | Can make installment billing easier to manage. |

| Bundling or multi-policy savings | Would another policy reduce the auto premium? | May reduce the total cost if the bundle is actually useful. |

| Vehicle safety features | Do anti-theft or safety features qualify? | Can help lower cost depending on insurer rules. |

4. Adjust Deductibles Carefully

Raising a deductible can lower the premium, but it also raises the amount you may need to pay after a claim. This can be a reasonable way to improve affordability only if the deductible is still realistic for your budget.

The Insurance Information Institute lists higher deductibles as one way to lower auto insurance costs, but the practical test is simple: the deductible should not be so high that a covered loss becomes unaffordable.[3]

5. Ask About Fees Before You Enroll

A low-upfront plan can become less affordable if it includes recurring billing charges. These can include installment fees, service fees, payment processing fees, returned-payment fees, late fees, cancellation fees, or reinstatement costs.

The most useful comparison is the total amount paid by the end of the term. If one quote has a lower first payment but higher monthly fees, another quote with a slightly higher startup payment may be cheaper overall. For a deeper fee breakdown, read BNPL car insurance fees to expect.

| Fee or Cost | Where It May Appear | Why It Matters | Question to Ask |

|---|---|---|---|

| Installment fee | Monthly bill or payment schedule. | Can raise the cost of paying over time. | Is this charged once or with every payment? |

| Service or processing fee | Checkout, payment portal, or billing terms. | May make the low first payment less valuable. | Is there a fee for card, online, or phone payments? |

| Late-payment fee | Billing agreement or late notice. | Can turn a manageable plan into an expensive one. | When is a payment considered late? |

| Returned-payment fee | Failed autopay or bank-return notice. | A failed payment can create extra charges and cancellation risk. | What happens if autopay fails? |

| Reinstatement cost | Cancellation or restart process. | Restoring coverage may cost more than staying current. | Can the policy be reinstated, and what would it cost? |

6. Protect Financed and Leased Vehicles

Drivers with financed or leased vehicles should be extra careful. A very cheap quote may not meet lender requirements if it only includes minimum liability coverage. Many lenders require collision and comprehensive coverage because they want the vehicle itself protected.

The CFPB explains that if coverage lapses on a financed vehicle, a lender may obtain force-placed insurance that protects the lender and vehicle rather than the driver personally.[4] That is why the best affordable policy is one you can keep active, not only one you can start.

Affordable But Safer Choices

- Compare at least three quotes using similar limits.

- Use discounts before removing important coverage.

- Choose deductibles you could realistically pay.

- Confirm lender requirements before buying.

- Keep proof of payment and policy documents.

Choices to Avoid

- Choosing the lowest first payment without checking total cost.

- Dropping coverages required by a lender or lease.

- Ignoring late-payment and cancellation rules.

- Accepting unclear fees or incomplete payment schedules.

- Picking a deductible that would be impossible to pay.

7. Compare Low-Upfront Plans Side by Side

The clearest way to choose affordable coverage without a large starting payment is to compare multiple low-upfront options next to a standard installment quote and a pay-in-full quote. That helps you see whether the flexible plan solves a cash-flow problem without costing too much more overall.

Buy Now Pay Later-style payment models are built around splitting costs into smaller payments over time. The CFPB has described BNPL as a form of credit that lets consumers split transactions into installments and repay over time.[5] Auto insurance billing is not always identical to retail BNPL, but the same practical caution applies: make sure the repayment schedule is realistic before choosing convenience over total cost.

1 Keep coverage equal

Compare liability limits, deductibles, and optional coverages as closely as possible. Otherwise, the cheapest quote may only be cheaper because it protects you less.

2 Add every payment and fee

Add the first payment, all scheduled payments, installment charges, service fees, and likely penalties. The full-term total gives you a more honest comparison than the amount due today.

3 Match the schedule to your income

A flexible plan only works if the later payments match your real budget. If the monthly schedule already feels tight, a slightly higher first payment with lower ongoing cost may be safer.

Questions to Ask Before Choosing Affordable No-Down-Payment Coverage

| Question | Why It Matters | Better Answer to Look For |

|---|---|---|

| What exact amount is due today? | Some low-upfront quotes still include startup fees or a first installment. | A clear total before coverage begins. |

| What is the full-term cost? | The first payment does not show the real policy cost. | A full payment schedule with every fee included. |

| Are the coverage limits the same across quotes? | One quote may look cheaper because it offers less protection. | Side-by-side limits, deductibles, and coverage types. |

| What fees apply to monthly billing? | Installment charges can raise the real cost. | Clear disclosure of installment, service, and processing fees. |

| What happens if I miss a payment? | Late fees and cancellation can create bigger problems later. | Clear grace period, late-fee, cancellation, and reinstatement rules. |

| Can discounts reduce the premium? | Discounts can improve affordability without simply delaying payment. | A quote that applies all eligible discounts before final comparison. |

Related BNPLCI Guides

FAQ

What does affordable no-down-payment car insurance mean?

It usually means finding a car insurance policy with a lower amount due at the start while still comparing the full premium, coverage limits, deductibles, fees, and payment schedule.

Is no-down-payment car insurance always cheaper?

No. It may reduce the amount due today, but the total cost can be higher if installment fees, service charges, or less favorable terms apply.

How can I lower the cost without weakening coverage too much?

Compare multiple quotes, ask about discounts, choose deductibles carefully, keep limits realistic, and review whether monthly billing adds extra charges.

Should I choose the lowest first payment?

Not automatically. The lowest first payment may not be the best choice if the monthly payments, total premium, deductibles, or cancellation rules are worse than another quote.

What should I check before starting coverage?

Check the amount due today, the effective date, the full payment schedule, coverage limits, deductibles, billing fees, late-payment rules, and cancellation or reinstatement terms.

Conclusion

Affordable no-down-payment car insurance can be useful when a large upfront cost is the main barrier to getting insured. The strongest choice is not always the quote with the smallest first payment. It is the quote that balances startup affordability, total cost, coverage strength, billing transparency, and payment terms you can realistically maintain.

Before choosing a low-upfront policy, compare the first payment, full-term premium, coverage limits, deductibles, discounts, installment fees, late-payment rules, and cancellation conditions. A flexible payment structure can help, but only when the policy remains affordable and useful after coverage begins.

References

- Insurance Information Institute — Auto Insurance Basics ↩

- NAIC — A Shopping Tool for Auto Insurance ↩

- Insurance Information Institute — Nine Ways to Lower Your Auto Insurance Costs ↩

- Consumer Financial Protection Bureau — Auto Insurance Options When Financing a Car ↩

- Consumer Financial Protection Bureau — Buy Now, Pay Later: Market Trends and Consumer Impacts ↩