Qualifying for BNPLCI is not about one universal approval rule. It depends on the insurer or financing arrangement behind the policy, your driving profile, the vehicle you want to insure, your state’s insurance requirements, and how the premium is billed. In other words, flexible payment options can make coverage easier to start, but they do not erase underwriting rules or state minimum coverage laws.

If you are still learning the basics, start with what buy now pay later car insurance is. Once you understand that BNPL-style coverage is mainly about how the premium is paid, it becomes easier to see what really affects eligibility and pricing.

What helps most

A manageable risk profile, accurate information, and a payment structure you can actually keep up with.

What carriers look at

Driving history, vehicle type, location, coverage choice, and sometimes credit-related factors where allowed.

What to avoid

Choosing a plan based only on the first payment and ignoring the total cost or payment rules.

Best mindset

Think in terms of approval plus long-term affordability, not approval alone.

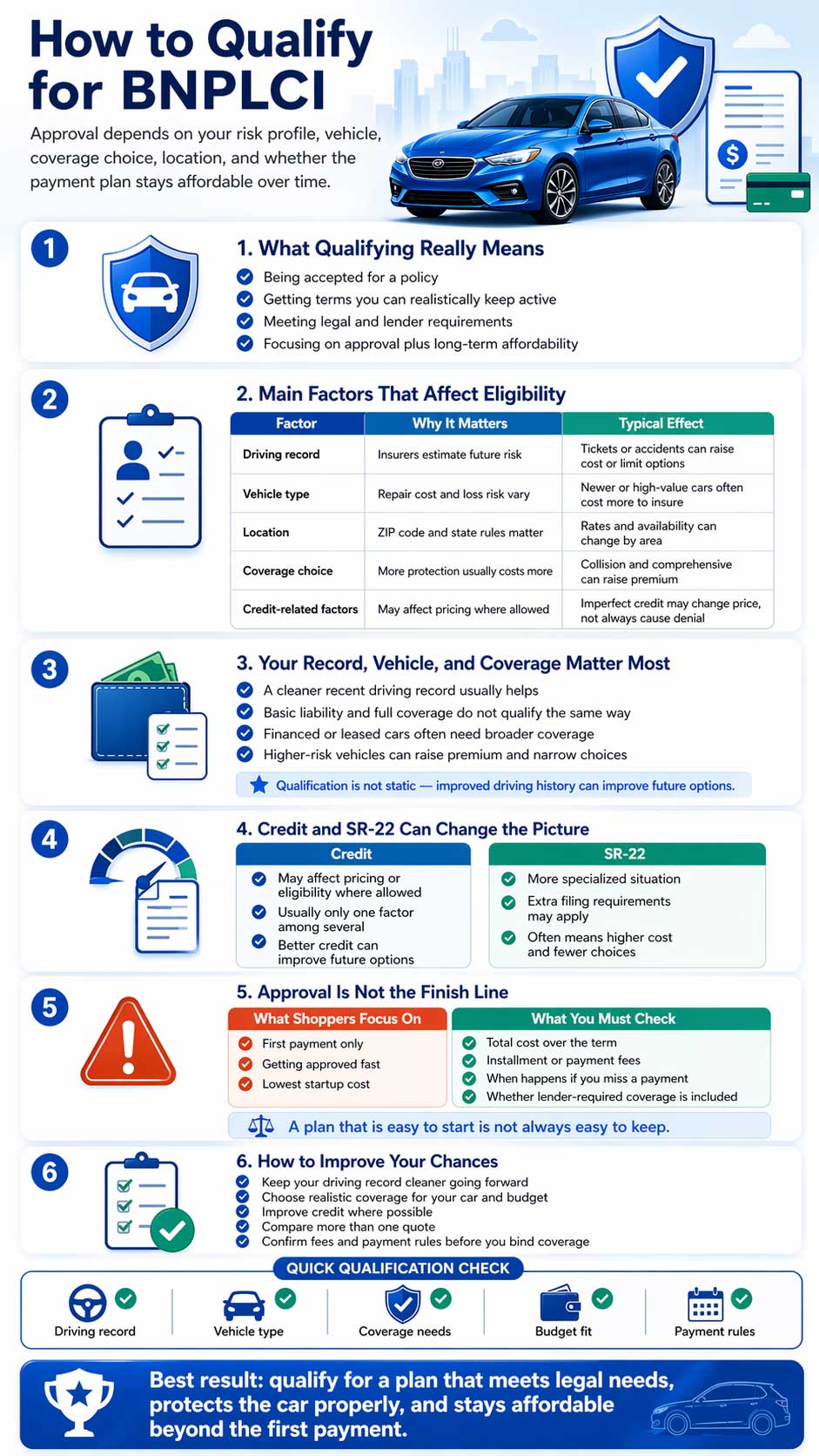

What “Qualifying” Really Means

For many drivers, “qualifying” means one of two things: first, being accepted for a policy at all, and second, being offered terms that are realistic enough to keep active. That distinction matters. A quote is not automatically a good fit just because it starts with a smaller upfront payment. The better goal is to qualify for a plan that meets your legal requirements, fits your car, and stays affordable month after month.

Because BNPL-style arrangements often involve installment billing or premium finance, you should think of them as a payment structure layered onto a standard auto policy, not as a completely separate class of insurance. For a broader payment comparison, see flexible payment plans at BNPLCI and buy now pay later car insurance options.

Main Factors That Affect Eligibility

| Factor | Why It Matters | How It Can Affect You |

|---|---|---|

| Driving record | Insurers use driving history to estimate future risk. | Tickets, accidents, and violations can raise premiums or narrow your options. |

| Vehicle type | Different vehicles create different repair costs and loss risks. | High-value, newer, or more expensive-to-repair vehicles can cost more to insure. |

| Where you live | Location affects claims patterns, theft exposure, and state requirements. | Rates and plan availability can vary by ZIP code and state. |

| Coverage selection | Minimum liability and broader physical-damage protection are priced differently. | Choosing collision and comprehensive usually raises cost but may be required on financed cars. |

| Credit-related factors where allowed | Some insurers use credit information in underwriting or rating, subject to state law. | Credit history may affect eligibility or pricing, but it is not the only factor. |

Maine’s insurance guidance explains that, where credit information is used, insurers may use it for underwriting or rating, but a premium is not based on credit history alone. Other factors can include your driving record, the type of car you drive, and where you live.[1] That makes BNPLCI qualification less about a single “yes or no” and more about how multiple risk factors work together.

Why Driving Record Still Carries So Much Weight

A clean driving record does not guarantee the cheapest plan, but it generally improves your position. Insurers use prior accidents, violations, and overall claims exposure to judge risk. Drivers with recent infractions may still find installment-friendly options, but the monthly cost can be higher and the terms can be tighter.

Practical takeaway: if your record has improved, shop again. Qualification is not static. A better recent record can open up better pricing and more flexible billing options than you had before.

If you are comparing your next move, it can help to review how BNPL car insurance providers compare instead of assuming all companies treat risk the same way.

Vehicle and Coverage Choices Can Change the Outcome

Qualification is also affected by what you are trying to insure. A lower-value car with basic liability-only coverage is a different risk from a newer financed vehicle that needs liability, collision, and comprehensive. Washington’s insurance guidance explains that collision pays for damage to your car after a crash, while comprehensive covers losses such as theft, vandalism, hail, fire, or animal impact. Those coverages often matter more when the vehicle is newer or financed.

| Coverage Choice | What It Usually Means | Qualification Impact |

|---|---|---|

| State-minimum liability | The lowest legal starting point in many states | Usually lowers premium, but may leave major gaps in protection |

| Liability + collision | Adds protection for crash damage to your car | Raises cost, especially for higher-value vehicles |

| Liability + comprehensive | Adds protection for theft, weather, and other non-collision losses | Can improve protection but increase premium |

| Full physical-damage package | Often means liability, collision, and comprehensive together | More expensive, but often necessary for financed or leased vehicles |

If you want to compare affordability with payment flexibility, read no down payment car insurance explained and affordable coverage without a down payment.

Credit History Can Matter, but It Is Not Everything

One of the weakest parts of the original article was treating credit like a simple pass-or-fail gate. That is not how the issue should be explained. Maine’s consumer guide says that if credit information is used, you should ask whether it affects eligibility, pricing, or both. It also notes that credit history is only one of several factors insurers may use.[1]

- Late payments and negative public records can hurt your insurance-related credit profile.

- A longer credit history can help in some scoring models.

- Improving your credit over time can improve future insurance options.

- Your premium is still influenced by non-credit factors like driving record, car type, and location.

That means drivers with limited or imperfect credit may still qualify, but the price and payment structure may change. The honest way to present BNPLCI is not “everyone gets the same flexible deal,” but rather “many drivers can still find options, though terms vary.”

SR-22 Can Change the Conversation

If you need an SR-22 filing, your situation is more specialized. California DMV explains that after certain DUI-related actions, a driver may be required to file a California Insurance Proof Certificate, listed as SR-22 or SR-1P, along with other reinstatement steps.[3] In practical terms, that means extra paperwork, a higher-risk profile, and often a more expensive policy.

Drivers who need SR-22 coverage can still shop for workable payment structures, but they should expect the filing requirement itself to narrow some options and raise cost. This is where comparing carriers carefully matters the most, because not every insurer handles higher-risk drivers the same way.

Why Payment Structure Matters After Approval

Qualifying is only the first step. The second step is qualifying for a plan you can actually keep. California DFPI explains that premium finance companies exist to advance money directly or indirectly to an insurer or producer under a premium finance agreement.[2] That is important because it confirms what BNPL-style insurance really is: often a financing or installment mechanism behind an otherwise standard policy.

A smaller amount due at the beginning can help a driver get insured sooner, but it can also mean more due dates, more chances for fees, and more pressure if your budget is already tight. That is why approval alone should never be the end of the comparison.

| Question | Why You Should Ask It |

|---|---|

| How much is due today? | The startup amount affects whether you can begin coverage now. |

| What is the total cost over the term? | This tells you whether the plan is actually affordable. |

| Are there installment or payment-related fees? | Small recurring fees can make a flexible plan cost more than expected. |

| What happens if I miss a payment? | This reveals lapse risk, reinstatement issues, and possible extra charges. |

| Does my lender require broader coverage? | Financed and leased vehicles often require more than minimum liability. |

Financed Cars Raise the Stakes

The CFPB warns that if you do not have insurance when buying a vehicle, or if your coverage later lapses, the lender can obtain force-placed insurance. That coverage protects the lender and the vehicle, but not you.[4] This is one of the strongest reasons to qualify for a plan you can maintain, not just one you can start.

If your budget is already tight, the risk of a lapse matters even more than the first payment. A policy that feels manageable on day one but becomes unstable after two or three months can create a more expensive problem later. For more on that side of the decision, see understanding BNPL risks.

How To Improve Your Chances

Keep your record cleaner going forward

Old issues cannot always be erased, but avoiding new tickets and claims helps future quotes.

Choose realistic coverage

Do not overbuy extras you do not need, but do not underinsure a financed or higher-value car either.

Improve credit where possible

Paying bills on time and reducing unresolved credit problems can help over time where credit is used.

Compare before committing

Different carriers weigh risk differently, so more than one quote matters.

- Gather accurate vehicle, driver, and address information before quoting.

- Ask whether the plan involves installment billing or premium finance.

- Confirm every fee category before you bind coverage.

- Review whether the plan still works if your budget gets tighter next month.

- Shop more than one quote instead of treating the first approval as the best option.

FAQ

Does BNPLCI guarantee approval for every driver?

No. Approval depends on the insurer or payment arrangement behind the quote, your risk profile, your state, the vehicle, and the coverage selected.

Is bad credit an automatic denial?

Not necessarily. Where credit is used, it may affect pricing or eligibility, but it is usually only one factor among several. Driving history, location, and vehicle type also matter.

Can I still qualify if I need SR-22?

You may still find options, but SR-22 situations are more specialized and often more expensive. Filing requirements and insurer appetite can narrow the choices.

What is the biggest mistake people make?

Many shoppers focus only on getting approved or on the first payment. The smarter move is to compare the full cost, the coverage, and how stable the plan will be over the full term.

Conclusion

Qualifying for BNPLCI is really about matching three things at once: your risk profile, the insurer’s underwriting rules, and a payment structure you can actually keep active. A clean record helps. A sensible coverage choice helps. Better credit can help where it is used. But the real win is not simply getting approved. It is getting approved for a plan that meets your legal needs, protects the vehicle properly, and fits your budget beyond the first payment.

Start with the right comparison

Before choosing a quote, compare how approval factors, coverage needs, and payment terms work together. Visit BNPLCI and review your options with the full cost in mind.

References

- Maine Bureau of Insurance — How Insurers Use Credit Information to Calculate Your Insurance Score for Personal Auto and Homeowners Insurance↩

- Maine Bureau of Insurance — Credit Information Guidance for Underwriting and Rating↩

- California Department of Financial Protection and Innovation — Insurance Premium Finance↩

- California DMV — DUI Convictions and SR-22 Filing Requirements↩

- Consumer Financial Protection Bureau — Auto Insurance Options When Financing a Car↩