Many drivers use the phrase no down payment car insurance when they are really looking for low upfront car insurance or a policy that starts with a smaller first payment. In practice, legitimate insurers usually require some payment before coverage becomes active. That first payment is generally part of your premium, not a separate bonus charge added on top.[3][4]

This distinction matters because it helps you compare quotes more accurately, avoid misleading offers, and choose a payment structure that fits your budget without overlooking the actual coverage you may need.

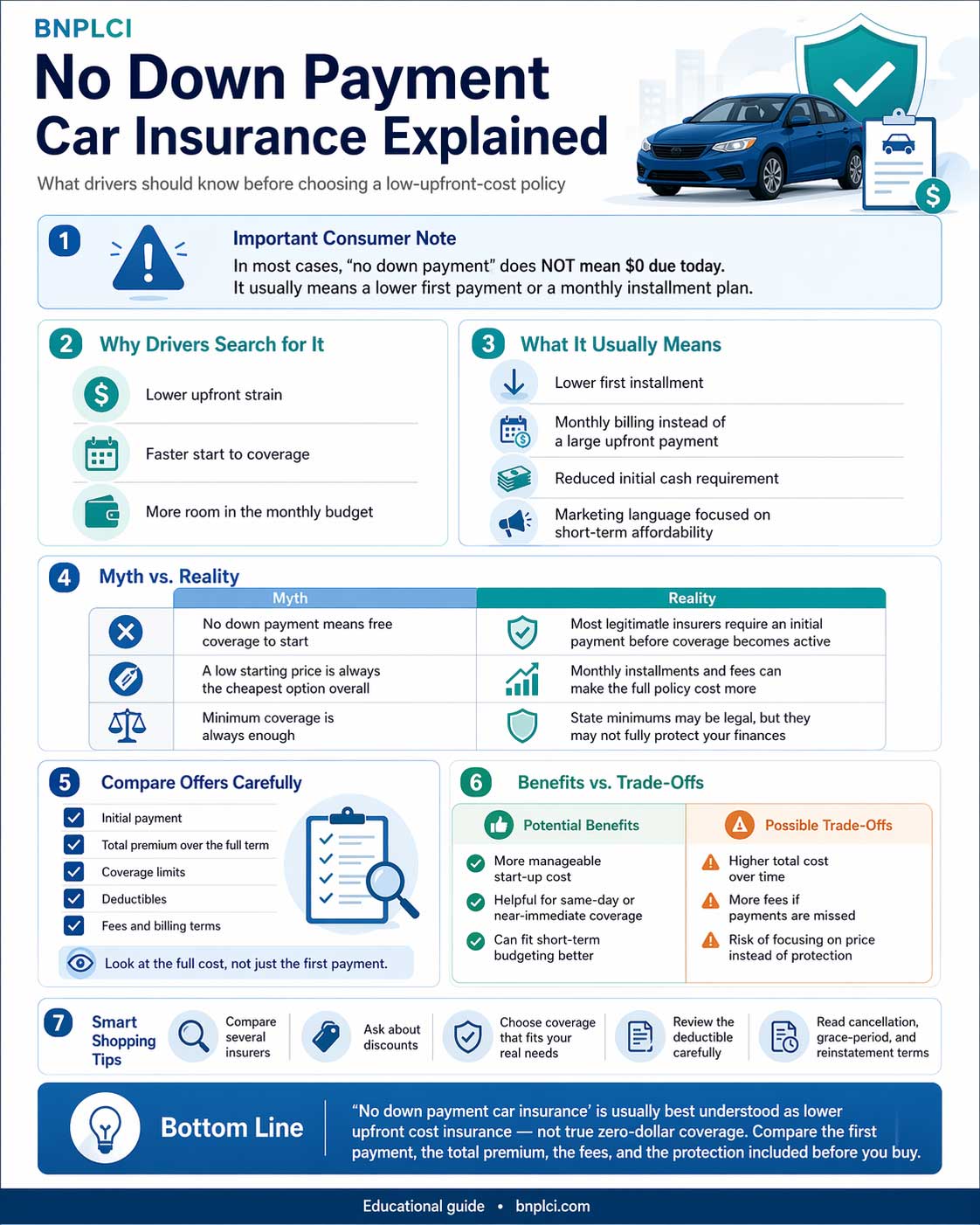

Car insurance is one of the most important costs that comes with owning a vehicle. If you are shopping for a new policy, you may have seen offers that sound like you can start driving with no money upfront. In reality, what most shoppers want is a way to begin coverage with a smaller initial payment while keeping the monthly cost manageable.

In simple terms, no down payment car insurance is often a marketing phrase used to describe a policy with a low first installment rather than a true zero-dollar start. The best way to evaluate these offers is to look past the headline and compare the full premium, the billing schedule, the fees, the deductible, and the actual protections included in the policy. If you are looking for a broader introduction to flexible upfront costs, this guide on affordable coverage without a down payment can help.

Why People Search for This Type of Policy

Lower Upfront Strain

A smaller first payment can make it easier to get insured without draining cash needed for fuel, registration, repairs, or other immediate expenses.

Faster Start to Coverage

Drivers often need coverage quickly to register a vehicle, comply with state rules, or avoid a lapse that could make later insurance more expensive.

More Room in the Budget

Some drivers prefer spreading costs out over time instead of paying a large amount immediately, even if the total yearly cost may not be lower.

What This Type of Offer Usually Means

Most of the time, the phrase does not mean that the insurer gives you active coverage for free at the start. It more often means one of the following: the first billed amount is lower than expected, the premium is split into monthly installments, the company has an installment plan that reduces the initial cash requirement, or the advertisement is using broad wording to attract drivers who are shopping by short-term affordability.

What to watch for: a small first payment can still lead to a higher total cost over the full policy term if installment fees, late fees, reinstatement fees, processing fees, low coverage limits, or high deductibles are part of the offer.

- A small first payment can still lead to a higher total cost over the full policy term.

- Installment fees, late fees, reinstatement fees, or payment processing fees may affect affordability.

- Minimum coverage may satisfy state rules but may not fully protect your finances after a serious accident.[1]

- If your car is financed or leased, the lender may require collision and comprehensive in addition to state-required liability insurance.

- A very cheap starting price should always be reviewed next to the deductible, exclusions, and coverage limits.

If you want a related explanation of how this connects to flexible payment models, you can also read what buy now pay later car insurance is.

Myth vs. Reality

| Common Myth | What Is Usually True | Why It Matters |

|---|---|---|

| “No down payment” means truly no money is due before coverage starts. | Most legitimate insurers require an initial payment before activating the policy. | You should compare the first payment and the total premium together. |

| A low starting price always means the policy is cheaper overall. | The monthly installments and added fees may make the full policy more expensive. | The best comparison is the total cost for the six- or twelve-month term. |

| Minimum coverage is always enough. | State minimums are legal baselines, not always strong financial protection. | Being underinsured can leave you paying large out-of-pocket costs after a claim. |

| Financed cars only need liability. | Many lenders require collision and comprehensive coverage. | Ignoring lender requirements can create loan or lease problems. |

How to Compare No Down Payment Car Insurance Offers

| Item to Compare | Why It Matters | Question to Ask |

|---|---|---|

| Initial payment | This affects how quickly you can start the policy and what you need to pay today. | Is this the first installment or a special fee structure? |

| Total premium | A lower opening payment does not automatically mean the policy is cheap overall. | What will I pay over the full term? |

| Coverage limits | Low limits may meet minimum rules but still leave major gaps. | Would these limits realistically protect me after a serious crash? |

| Deductibles | A higher deductible can lower the premium but increase your out-of-pocket risk. | Could I afford this deductible if I had to file a claim? |

| Fees and billing terms | Installment charges and late fees can change the real cost of the policy. | Are there monthly service fees, reinstatement fees, or cancellation fees? |

Benefits and Trade-Offs

Potential Benefits

- More manageable start-up cost

- Helpful when you need same-day or near-immediate coverage

- Can fit better into short-term budgeting

Possible Trade-Offs

- Higher total cost over time

- More fees if you miss payments

- Risk of focusing on price instead of protection

How to Improve Your Chances of Finding a Better Offer

- Compare quotes from several insurers instead of choosing the first ad you see.

- Ask about discounts for bundling, autopay, paperless billing, good driving, or multi-car policies.

- Choose only the coverages you actually need, while still meeting state and lender requirements.

- Review the deductible carefully so a lower premium does not create a painful claim later.

- Read policy terms before paying, especially around cancellations, grace periods, and reinstatement.

For more practical guidance before applying, review these tips on qualifying for flexible payment options.

FAQ

Is no down payment car insurance really available?

Usually not in the literal sense. In most cases, drivers are finding policies with lower upfront costs or monthly billing rather than a true zero-dollar start.

What coverage do these policies usually include?

That depends on the insurer and your state, but many policies start with liability coverage. Some drivers also add collision, comprehensive, uninsured motorist coverage, medical payments, or personal injury protection where applicable.

Can a lower initial payment save money overall?

Not always. A smaller first payment may help with immediate affordability, but the total premium and any installment fees may still make the policy more expensive over time.

Why should financed drivers be extra careful?

If your car is financed or leased, your lender may require physical damage coverage such as collision and comprehensive, so the cheapest quote may not meet all your obligations.

What is the biggest mistake shoppers make?

Looking only at the opening payment. A better comparison looks at the full premium, coverage limits, deductible, fees, exclusions, and the insurer’s billing terms.

Conclusion

No down payment car insurance is best understood as a search for lower upfront costs, not as free same-day coverage with no payment due. The right policy is the one that helps you start legally, fits your budget, and still gives you protection that makes sense for your state, your vehicle, and your financial situation.

If you are comparing flexible payment options, use the headline offer as a starting point, then look deeper at the total cost, the billing structure, and the actual coverage. For more educational guides and comparison-focused content, visit BNPLCI.