BNPL car insurance providers can look similar at first because many advertise quick approvals, smaller starting payments, and flexible terms. The real differences usually show up in the parts people skim past: how the billing schedule works, what fees apply if something goes wrong, which discounts you can actually use, and how easy the provider is to deal with after enrollment.

The smartest comparison is not just about finding the lowest first payment. It is about matching the right coverage to a payment structure you can realistically maintain. If you are still deciding between billing styles, start with BNPL vs. traditional car insurance so you can separate payment flexibility from actual policy protection.

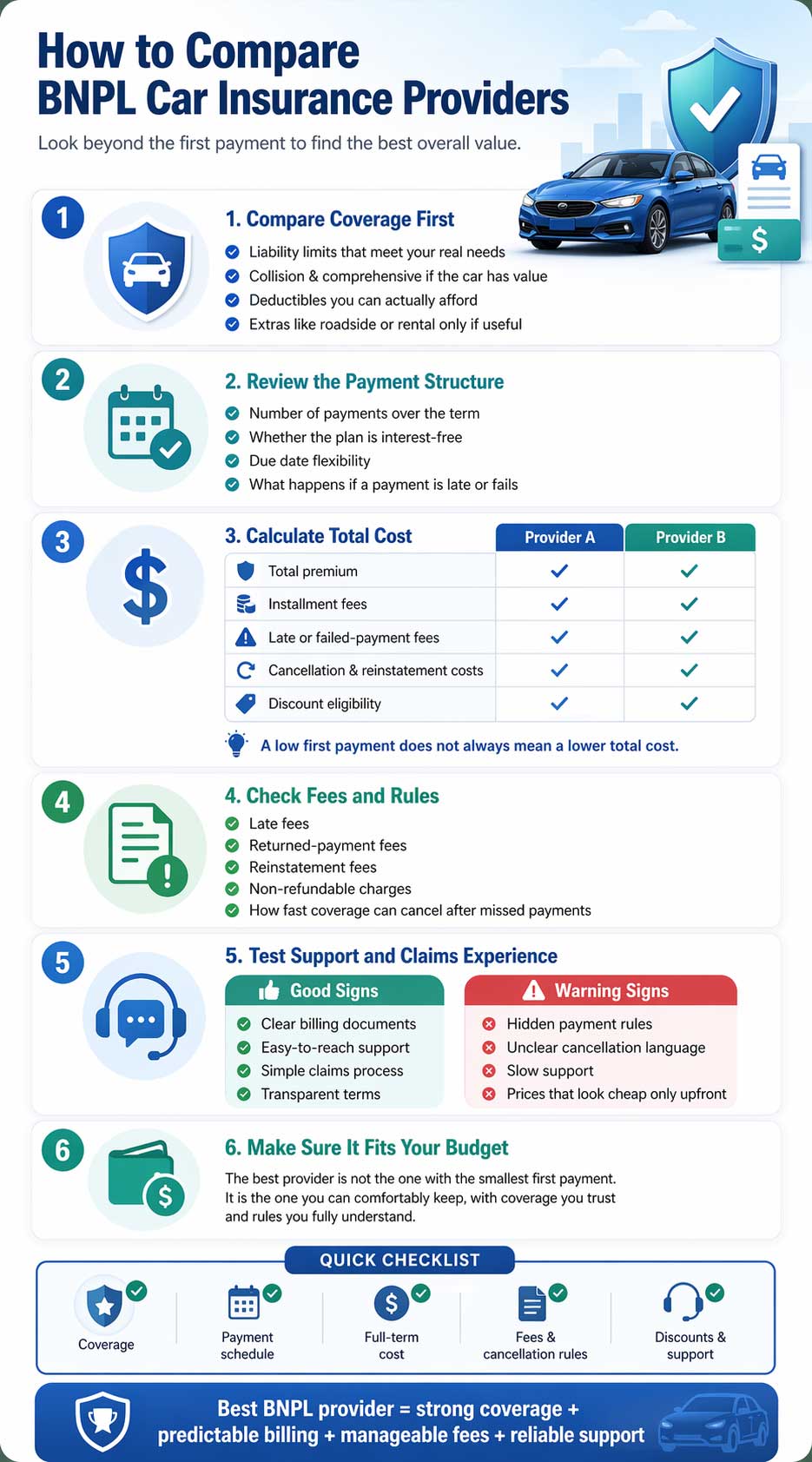

Compare Coverage First

A flexible plan is only useful if the underlying liability limits, deductibles, and optional protections still fit your real needs.

Compare Total Cost

A smaller amount due today does not always mean the provider is cheaper over the full term.

Compare Rules

Late fees, failed-payment handling, cancellation timing, and reinstatement rules can change the value of a plan quickly.

Start With Coverage First, Not the Payment Plan

BNPL changes how you pay, not what auto insurance is supposed to protect. Before you compare providers, decide what coverage you actually need. That usually means reviewing liability limits, deductibles, collision and comprehensive needs, and any extras such as roadside assistance or rental reimbursement.[1]

- Liability coverage: the legal foundation in most states and often the most important place to avoid going too low.

- Collision and comprehensive: more relevant if your vehicle has enough value that you would struggle to replace it out of pocket.

- Deductibles: lower deductibles mean more protection at claim time, but usually a higher premium.

- Optional extras: only add value if you would realistically use them.

Compare the Payment Structure Carefully

Not all BNPL-style insurance billing works the same way. Some plans feel like short installment cycles, while others function more like standard monthly payments with a lighter starting burden. That is why you should compare the actual payment rhythm, not just the marketing language.[3]

Questions to Ask Every Provider

- How many payments will I make over the term?

- Is the plan truly interest-free, and under what conditions?

- Can I change the due date if it does not match my payday?

- What happens if a payment fails or is delayed?

What Good Billing Looks Like

- Clear due dates shown before you enroll.

- Straightforward fee disclosures.

- Reasonable handling of failed or late payments.

- A schedule that matches your actual cash flow.

Always Compare Total Cost, Not Just the First Month

Low monthly pricing can be misleading if you only look at the first payment. A plan may feel cheaper upfront but cost more once installment charges, billing fees, or penalties are added. You should compare the full cost across the term and also look at what happens if you cancel early or miss a payment.[2]

If you want a focused breakdown of where extra charges usually appear, review hidden fees in BNPL car insurance and keep BNPL car insurance fees: what to expect open while you compare providers.

| What to Compare | Why It Matters | What to Ask |

|---|---|---|

| Total premium | A low first payment does not tell you the full cost. | What will I pay over the entire term? |

| Installment fees | Monthly convenience can quietly raise the total price. | Is there a charge for paying over time? |

| Late and failed-payment fees | One bad month can make the plan much more expensive. | What happens if a payment is late or declined? |

| Cancellation and reinstatement rules | These rules affect what happens when coverage is interrupted. | How fast can a policy cancel, and what does it cost to restore it? |

| Discount eligibility | Discounts can completely change which provider is the best value. | Which discounts apply to me right now? |

Verify Fees, Penalties, and Cancellation Rules

Fees are often the make-or-break part of a BNPL comparison. A provider with clear terms and manageable penalties may be far better than one with a cheaper-looking first payment but aggressive billing rules. Always confirm:

- Late payment fees

- Returned or failed payment fees

- Reinstatement fees

- Non-refundable charges

- How quickly the policy can cancel after missed payments

Check the Discounts You Can Actually Use

Discounts can change the ranking of providers fast. Ask for a list of discounts and confirm which ones apply to your profile instead of assuming they are automatic. For younger or newer drivers, it helps to review car insurance discounts for young drivers before comparing quotes side by side.[5]

Common discount areas to ask about include student status, driver training, telematics, safety features, low mileage, autopay, and multi-car eligibility.

Test the Claims Experience and Support Before You Buy

Price matters, but service matters too. A provider with confusing billing support or weak claims handling can create extra stress when you actually need help. Before you choose, look at whether the provider is easy to reach, how documents are submitted, how billing disputes are handled, and how clearly policy changes are explained.

Signs of a Strong Provider Experience

- Easy-to-find billing and policy documents.

- Clear explanations of terms and fees.

- Fast response options by phone, chat, or email.

- Simple document upload and claims processes.

Warning Signs

- Hard-to-find payment rules.

- Unclear cancellation language.

- Support that is slow or difficult to reach.

- Pricing that looks low only because the real fees appear later.

Make Sure the Plan Fits Your Real Budget

BNPL is safest when the installments still feel manageable if something in your month changes. A payment plan that is already tight can become expensive fast after one missed payment. If you are unsure whether the schedule fits your cash flow, do a reality check with Is BNPL right for your budget?.[4]

FAQ

What is BNPL car insurance?

It usually refers to a payment structure that lets you spread policy costs over time instead of making a larger payment at the start.

How do I find the best BNPL car insurance provider?

Compare coverage first, then total cost, fee rules, discount eligibility, and the provider’s claims and billing support experience.

Are there extra fees with BNPL plans?

Sometimes. Common examples include installment charges, late fees, failed-payment fees, and reinstatement costs, depending on the provider.

Is BNPL a good option for first-time drivers?

It can be, but only if the payment schedule fits your budget and the policy still provides the coverage you actually need.

Key Takeaways

Compare coverage first, then payment structure. Always price the full term, verify fees and cancellation rules, confirm the discounts you truly qualify for, and favor providers with a solid support experience over ones that only look cheap on the first screen.