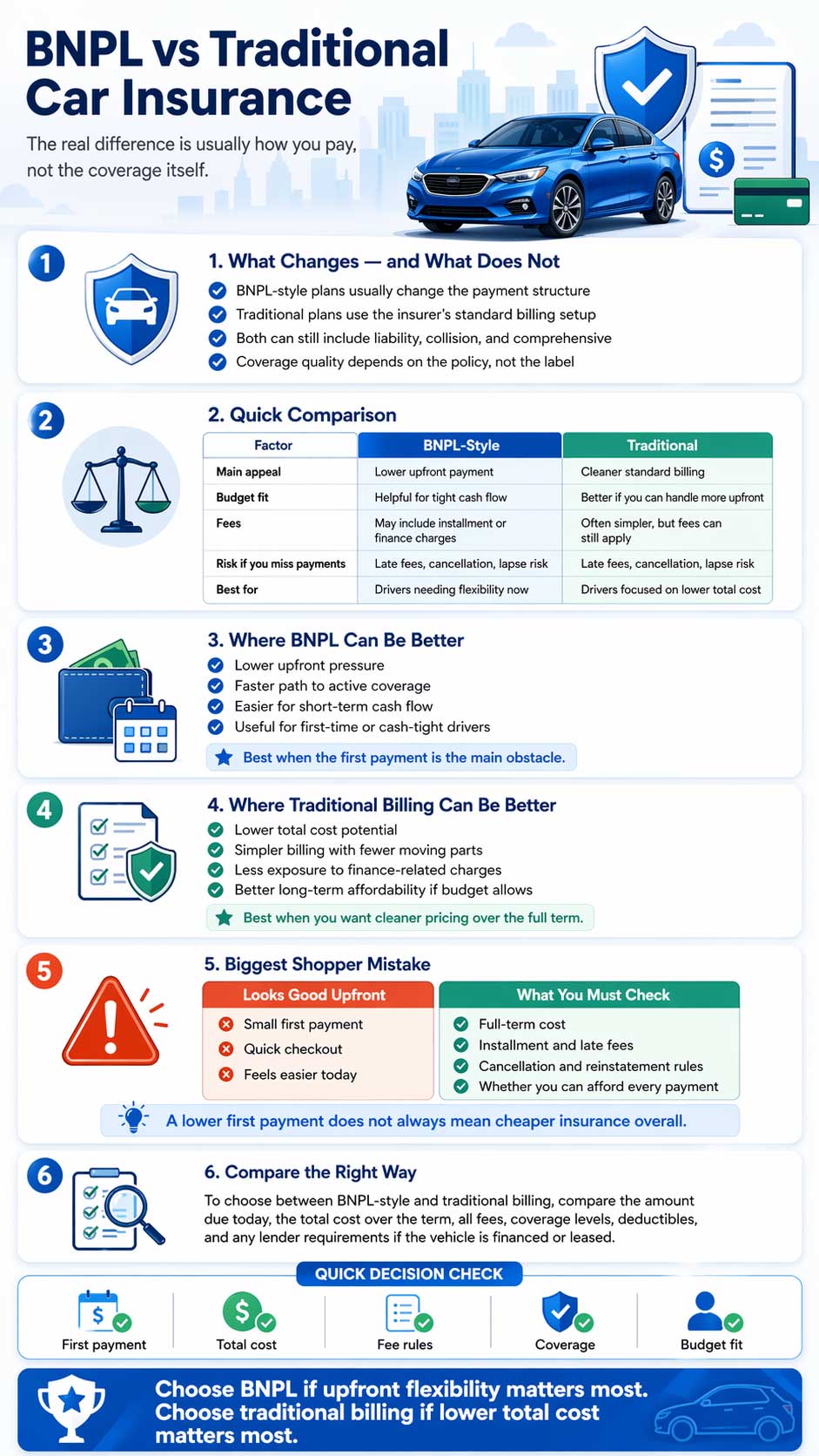

When people compare BNPL car insurance with traditional car insurance, they are usually comparing how the premium is paid, not two completely different legal categories of coverage. In most cases, BNPL-style auto insurance is best understood as a flexible payment approach built around smaller installments, while traditional car insurance usually refers to the standard billing structure offered by insurers. The policy itself can still include liability, collision, comprehensive, uninsured motorist protection, deductibles, and optional add-ons either way.

If you are new to the concept, it helps to first read what buy now pay later car insurance means. From there, the real question becomes simple: is it better to lower the amount due today, or to focus on the lowest total cost over the full policy term? That is where BNPL-style plans and traditional billing can start to feel very different.

BNPL-style setup

Usually aims to reduce upfront pressure by spreading costs into smaller payments over time.

Traditional billing

Usually follows the insurer’s standard payment structure, which may still allow installments but often puts less emphasis on payment flexibility.

What matters most

Look at the first payment, total cost, fees, due dates, cancellation rules, and whether the policy remains affordable all term long.

Quick Comparison Table

| Factor | BNPL-Style Car Insurance | Traditional Car Insurance |

|---|---|---|

| Main appeal | Lower upfront payment | Cleaner standard billing structure |

| Monthly budgeting | Often easier for tight cash flow | Can still be manageable, but may require more upfront |

| Fees | May include installment or finance-related charges [1][2] | May still include fees, but the structure is often simpler [2] |

| Coverage quality | Depends on the policy selected, not the payment label | Depends on the policy selected, not just the billing method |

| Risk if you miss payments | Can trigger fees, cancellation, or gaps in coverage [3][4] | The same risk exists if a standard policy is not paid on time [3][4] |

What BNPL Car Insurance Really Means

One of the biggest misunderstandings online is the idea that BNPL car insurance is some entirely separate form of insurance. In reality, the better way to look at it is as a payment structure. California’s DFPI explains that premium finance companies exist to advance money directly or indirectly to an insurer or producer at the request of the insured under a premium finance agreement. [1] That means the customer gets the policy in place, while the cost is handled over time through installments or financing arrangements.

So when a driver chooses BNPL-style coverage, they are often choosing payment flexibility more than a different protection package. This can be helpful for people who need immediate proof of insurance, want to preserve cash flow, or simply cannot absorb a larger upfront bill. But payment flexibility should never be confused with lower total cost. Smaller payments can feel easier, while still costing more by the end of the term once fees and finance charges are counted. [2]

How Traditional Car Insurance Usually Works

Traditional car insurance usually means the standard policy and billing options offered directly by insurers. That does not automatically mean “pay in full only.” Some traditional insurers still allow monthly or other installment arrangements. The key difference is that the product is presented primarily as an insurance policy first, while BNPL-style offers are often presented first as a budgeting solution.

This is why the smartest comparison is not “modern versus old.” It is cash-flow flexibility versus total-cost discipline. Traditional billing can be the better option for drivers who want fewer moving parts, clearer due dates, and less exposure to finance-related charges. BNPL-style billing can be the better option for drivers who need coverage now and need the first payment to stay manageable.

Where BNPL Can Be Better

- Lower upfront pressure: Helpful when paying a large amount at the beginning would strain your monthly budget.

- Faster path to active coverage: Useful for drivers who need to get insured right away for legal driving or registration reasons.

- Easier budgeting: Smaller scheduled payments may feel more realistic for households managing multiple bills at once.

- More flexibility for first-time or cash-tight drivers: The lower entry cost may make it easier to stay insured at the start.

That is why many drivers exploring flexible plans also end up reading about whether buy now pay later is right for them. If the main problem is upfront affordability, BNPL-style billing may solve a real short-term issue better than a traditional setup.

Where Traditional Billing Can Be Better

- Lower total cost potential: Fewer installment or finance-related charges can make the full term cheaper. [2]

- Simpler billing: There may be fewer extra fees, fewer third-party arrangements, and less chance of confusion.

- Stronger long-term affordability: If you can comfortably handle a larger first payment, you may reduce future payment stress.

- Less risk of payment stacking: Drivers sometimes underestimate how multiple future installments can crowd the monthly budget.

Traditional billing often works best for drivers who are focused on the entire premium, not just the first amount due. A quote that looks a little harder today can still be the smarter choice if it reduces charges over the next six or twelve months.

The Biggest Risk: Focusing Only on the First Payment

A low amount due today can be attractive, but it is not the same as truly affordable insurance. California’s insurance guidance notes that auto insurers may charge a range of fees, including installment fees, cancellation fees, reinstatement fees, late fees, and premium finance revenues or installment finance charges. [2] Those details matter because they change the real cost of the policy even when the initial payment looks small.

That is also why shoppers should not ignore the downside of missed payments. Maine’s Bureau of Insurance explains that premiums may be higher if prior coverage lapsed while the driver was required by law to carry insurance. [4] Washington’s insurance regulator also warns that if you do not maintain required coverage on a financed or leased vehicle, the lender can buy coverage to protect its own interest and charge you for it. [3]

If you want to go deeper on that side of the topic, this page pairs well with understanding BNPL risks. A flexible payment plan only helps if it is flexible enough for your real budget month after month.

BNPL vs. Traditional Car Insurance for Financed Vehicles

If your car is leased or financed, the comparison becomes even more important. Washington’s Office of the Insurance Commissioner states that most lenders require comprehensive and collision coverage on financed or leased vehicles. [3] That means the cheapest-looking payment option may not be enough if it only seems affordable because the driver is underestimating how much full coverage will actually cost over time.

In these situations, drivers should compare the full monthly commitment, not just the startup amount. A lapse can create bigger problems than just losing your policy. It can lead to lender-placed protection, added expense, or a worse insurance situation later. So the best option is usually the one that keeps the policy active reliably while still meeting lender requirements.

How to Compare the Two the Right Way

| What to Compare | Why It Matters |

|---|---|

| Amount due today | Shows whether you can realistically start the policy now |

| Total amount paid over the term | Reveals whether smaller payments actually cost more overall |

| Installment, late, cancellation, and reinstatement fees | These can turn a “cheap” plan into an expensive one. [2] |

| Coverage levels and deductibles | The payment method does not replace the need for proper protection |

| Lender requirements | Financed vehicles often require more than minimum liability. [3] |

Once you compare plans that way, the choice usually becomes clearer. If you still need help narrowing it down, the next best step is to compare BNPL car insurance providers side by side instead of judging by marketing language alone.

FAQ

Is BNPL car insurance a different kind of auto policy?

Usually not. It is more accurate to treat it as a payment-focused arrangement rather than a separate legal category of coverage. The underlying policy can still include standard auto insurance protections. [1][3]

Is BNPL always cheaper?

No. It may reduce the amount due upfront, but the total cost can be higher once installment fees, finance-related charges, or late fees are added. [2]

Can traditional car insurance still offer monthly payments?

Yes. Traditional billing does not always mean paying the full premium at once. Some insurers still offer installments, but the structure and cost details vary by company.

Final Takeaway

BNPL vs. traditional car insurance is really a decision about payment flexibility versus overall cost control. BNPL-style plans can be a smart choice when the priority is getting insured now without a heavy upfront hit. Traditional billing can be a smarter choice when the priority is reducing charges and keeping the total price cleaner over the full term. The best option is the one that gives you the right coverage, fits your real monthly budget, and helps you avoid a lapse that could cost even more later.

References

- California Department of Financial Protection and Innovation — Insurance Premium Finance ↩

- California Department of Insurance — Prior Approval Rate Filing Instructions ↩

- Washington Office of the Insurance Commissioner — Learn How Auto Insurance Works ↩

- Maine Bureau of Insurance — A Consumer’s Guide to Personal Auto Insurance ↩