Buy Now, Pay Later can be useful when it helps you avoid a large upfront bill, but its biggest risks usually show up after checkout. The problem is rarely one giant mistake. It is more often a series of smaller obligations, due dates, and fees that start to pile up until your budget feels tighter than expected. That is why payment structure matters just as much as the headline price.[1][2]

If you are using BNPL for insurance-related costs, the first step is understanding how flexible billing compares with more traditional payment setups. A useful starting point is BNPL vs. traditional car insurance, because the safest choice is not always the one with the smallest first payment.

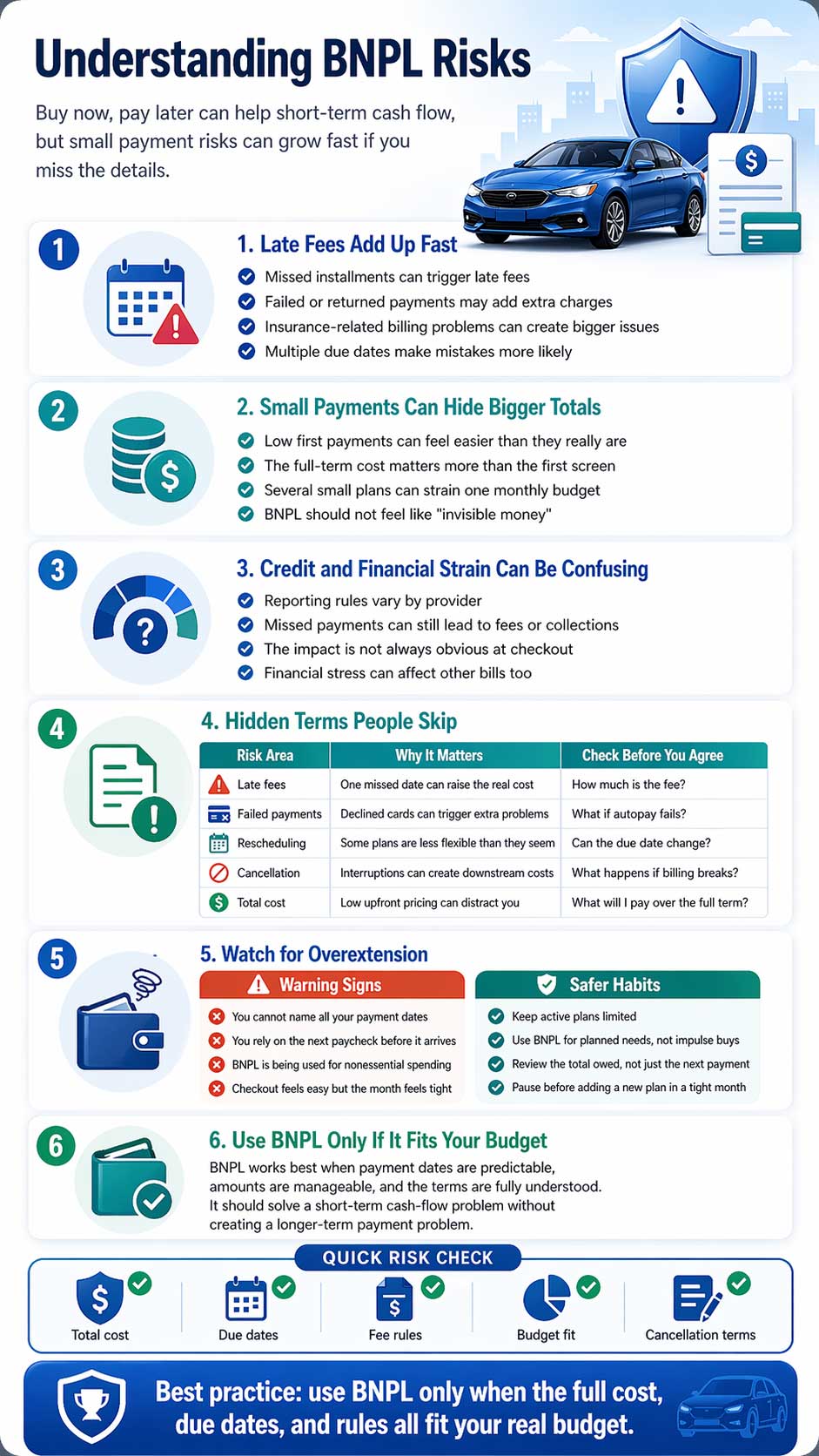

Late Fees Add Up Fast

A missed installment can turn a convenient plan into an expensive one, especially when multiple due dates overlap.

Small Payments Hide Bigger Totals

BNPL can feel harmless because each payment looks manageable on its own, even when the combined monthly total is not.

Terms Matter More Than Marketing

“No interest” does not mean no risk. The real cost is often buried in late-payment, failed-payment, and cancellation rules.

What BNPL Actually Is and Why It Can Get Risky

Most BNPL plans split a purchase into several payments. That sounds simple, but the risk rises when you have multiple plans active at the same time or when the due dates do not line up well with your paycheck. CFPB reporting has repeatedly highlighted that consumers can run into trouble when repayment obligations feel manageable separately but become harder to track together.[1][2]

BNPL can still be helpful. It may prevent a lapse in coverage, reduce pressure from a large upfront payment, or give you more room in a tight month. But those benefits only hold up if the installments remain realistic after your other bills are paid.

Risk 1: Late Payments That Trigger Fees

The most common BNPL problem is missing a payment. That often happens not because a person forgot the product existed, but because they are juggling several bills with different due dates. Once a payment is missed, late fees, returned-payment charges, or policy problems can follow quickly.

If you want to reduce this risk, keep BNPL car insurance fees: what to expect open before you enroll, and compare it with hidden fees in BNPL car insurance so you know what to watch for in the fine print.

Risk 2: Overspending Because It Does Not Feel Like Debt

One reason BNPL can be risky is psychological. A smaller first payment makes a purchase feel lighter, even when the full obligation is still substantial. That can lead people to underestimate how much they already owe across different plans. Experian notes that BNPL arrangements and related reporting practices can affect consumers differently depending on provider behavior and repayment patterns, which is another reason to avoid treating BNPL like “invisible money.”[3]

Signs You May Be Overextending

- You have trouble naming all of your active payment dates.

- You are using BNPL for nonessential spending repeatedly.

- You feel relief at checkout but stress later in the month.

- You are relying on your next paycheck before it arrives.

Safer Habits

- Keep the number of active plans low.

- Use BNPL for planned expenses, not impulse purchases.

- Review the total owed, not just the next installment.

- Pause before adding a new plan if your month already feels tight.

Risk 3: Credit Score Confusion

Credit impact is one of the areas that confuses people most. Some BNPL activity may be reported, some may not be, and provider practices can evolve. The safest assumption is that missed payments can still create consequences through fees, collections, or broader financial strain, even when the credit effect is not obvious at the start.[2][3]

If this is a major concern for you, review how BNPL affects your credit score. It matters even more if you are planning to finance a vehicle, move into a rental, or shop for lower insurance rates soon.

Risk 4: Hidden Terms People Skip

BNPL promotions often emphasize easy access and low upfront cost. What people miss are the details around failed-card payments, rescheduling rules, partial refunds, cancellation timing, and non-refundable charges. Even when the terms are technically disclosed, they are easy to rush past in a fast checkout flow.

| Risk Area | Why It Causes Problems | What to Check Before You Agree |

|---|---|---|

| Late fees | One missed date can raise the real cost quickly. | How much is the fee, and when does it apply? |

| Failed payment handling | Declined cards or bank issues can trigger extra charges or interruptions. | What happens if autopay fails? |

| Rescheduling rules | Some plans are less flexible than they look at checkout. | Can the due date be changed if needed? |

| Cancellation or reinstatement | Insurance-related billing issues can create bigger downstream costs. | What happens if the plan or policy is interrupted? |

| Total plan cost | Low upfront pricing can distract from the full obligation. | What will I pay over the full term? |

How to Manage BNPL More Safely

BNPL is safest when you treat it like a fixed budget item, not an easy extra. The goal is to make payments predictable enough that they do not start interfering with rent, utilities, insurance, or other essentials.

- Keep active plans limited. Fewer payment schedules are easier to manage accurately.

- Align due dates with your payday. If the provider allows date changes, use that option strategically.

- Use reminders or autopay. A missed payment is often avoidable with better timing tools.

- Use BNPL for needs, not impulse wants. Planned use is much safer than emotional use.

- Review the total monthly burden. Look at all active plans together, not one at a time.

When BNPL Can Make Sense for Insurance

BNPL can be a useful bridge if you need coverage now and you know the installments fit comfortably into your budget. But if the plan only solves the first payment while making the rest of the term harder to manage, it may not be the best option.[4]

In some cases, comparing alternatives such as no down payment car insurance may be more practical than focusing only on payment timing. If you are unsure whether BNPL matches your finances, use Is BNPL right for your budget? as a quick reality check.

FAQ

What are the most common BNPL risks?

The biggest ones are late fees, stacked payment obligations, confusing terms, and budget strain that spills into other bills.

How can I avoid debt problems when using BNPL?

Keep the number of active plans low, use BNPL for planned essentials only, track due dates carefully, and check the full monthly burden before adding another payment plan.

Is BNPL better than using a credit card?

It depends on the product, the fees, and your repayment habits. The safer option is usually the one with clearer terms and a payment structure you can comfortably manage.

Can late BNPL payments affect my credit?

They can, depending on the provider and what happens after the missed payment. Even when direct reporting is unclear, fees or collections can still create financial damage.

Bottom Line

BNPL is best used as a controlled financial tool, not as an automatic solution. If you keep plans limited, read the fee rules carefully, and make sure the payment schedule fits your real budget, you can lower the chance that convenience turns into stress.