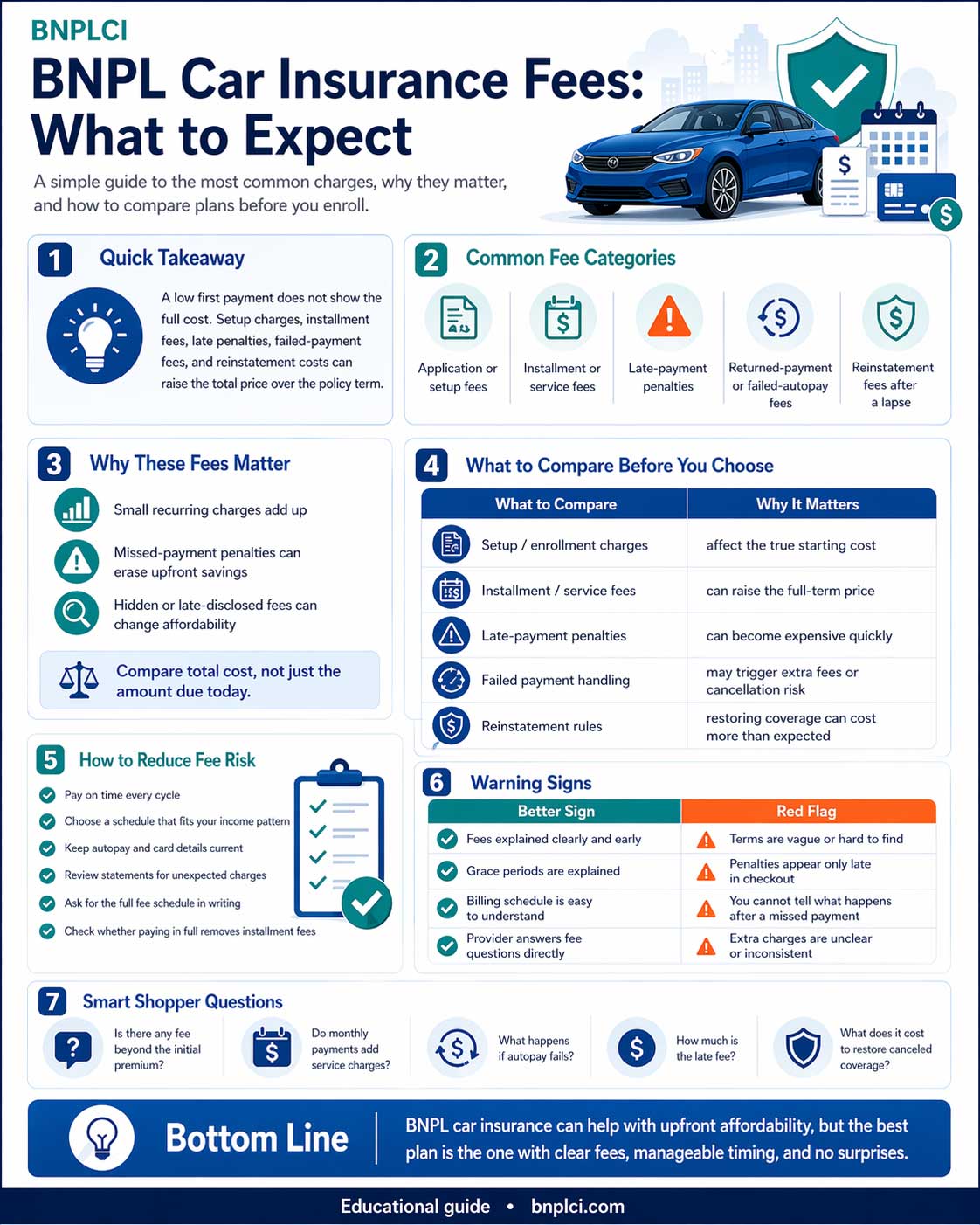

BNPL car insurance fees are the extra charges that may appear when an auto insurance policy is paid over time instead of paid mostly upfront. These fees can appear before coverage starts, during monthly billing, after a late or failed payment, or when a canceled policy must be reinstated.

This guide focuses on expected fee stages, not hidden fees. The goal is to help you compare the first payment, full-term premium, installment charges, late-payment rules, returned-payment fees, cancellation timing, and reinstatement costs before choosing a flexible car insurance payment plan.

The lowest amount due today is not always the cheapest policy overall. Auto insurance should still be compared by coverage limits, deductibles, total premium, billing rules, company reliability, and the full payment schedule.[1]

Before Coverage Starts

Expect to verify the first amount due, setup charges, payment method rules, and whether any fee is refundable.

During Billing

Installment, service, convenience, or processing fees may affect the real cost of spreading payments over time.

After Payment Problems

Late, failed-payment, cancellation, lapse, or reinstatement charges can appear if the payment schedule is interrupted.

When BNPL Car Insurance Fees May Appear

A BNPL-style auto insurance plan can make coverage easier to start because the first amount due may be lower than a traditional upfront payment. The tradeoff is that the total cost can depend on several fee categories. Some fees appear when the policy begins. Others appear each month. Some only appear if a payment is late, returned, or missed.

The table below separates the main fee stages so the page stays focused on what a driver should expect, where the fee may appear, and what to ask before enrolling. This keeps the purpose different from a hidden-fee guide. Here, the focus is the normal timeline of charges that can affect a pay-over-time insurance plan.

| Stage | Fee to Expect | Where It May Appear | What to Ask Before Choosing |

|---|---|---|---|

| Quote or Signup | Application, setup, enrollment, or payment-plan fee | Quote screen, checkout page, agency paperwork, or billing agreement | Is this fee part of the premium, separate from the premium, or refundable? |

| Policy Activation | First installment, initial premium, taxes, or required startup payment | Amount due today before coverage starts | What exact amount must be paid before the policy is active? |

| Monthly Billing | Installment, service, convenience, or processing fee | Billing schedule, monthly invoice, or payment portal | Is this charged once, monthly, or with every payment? |

| Autopay or Card Payment | Card processing, returned-payment, failed-autopay, or bank-return fee | Payment method terms, failed payment notice, or billing agreement | Can one failed payment trigger both a fee and a cancellation notice? |

| Late Payment | Late fee or penalty | Billing terms, late notice, or cancellation warning | When is the payment considered late, and is there any grace period? |

| Cancellation or Lapse | Cancellation, short-rate, reinstatement, or restart fee | Cancellation notice, reinstatement offer, or revised bill | What does it cost to restore coverage if the policy cancels? |

| Policy Changes | Endorsement, document, broker, or administrative fee | Policy change confirmation or agency invoice | Are there charges for changing vehicles, drivers, addresses, or coverage? |

Fees Before Coverage Starts

The first fee stage happens before the policy is active. A driver may see an application fee, setup fee, agency fee, enrollment fee, payment-plan charge, or first installment. These charges matter because they decide whether the advertised “low upfront” option is actually affordable today.

The most important question is simple: what exact amount must be paid before coverage begins? If the quote separates premium, taxes, installment charges, and agency fees, compare the full amount due today instead of only the monthly number displayed in the ad.

- Ask whether the startup fee is part of the premium or separate from it.

- Ask whether any application, agency, or enrollment fee is refundable.

- Confirm the policy effective date before driving.

- Save the quote, billing schedule, payment confirmation, and proof of insurance.

Fees During Monthly Billing

The second fee stage happens after coverage starts. Many flexible payment plans divide the premium into scheduled installments, but monthly billing may include installment, service, convenience, or processing charges. A small fee can look harmless on one bill, but it can add up across a six-month or twelve-month term.

Some insurance regulators have addressed installment premium payment plan fees, which shows that fees tied to installment billing are a real issue to review rather than a minor detail. Rules vary by state and by insurer, so the safest approach is to ask for the full billing schedule before agreeing to the policy.[2]

Charges to Look For

- Monthly installment fee.

- Payment processing fee.

- Convenience fee for card payments.

- Paper billing or document fee.

- Broker or agency service fee.

What to Compare

- Total premium with fees included.

- Monthly payment amount after all charges.

- Whether autopay lowers or removes a fee.

- Whether paying in full avoids installment charges.

- Whether fees are shown clearly before signup.

Fees After a Late or Failed Payment

The third fee stage appears when a scheduled payment does not go through on time. This is where a flexible plan can become expensive quickly. A missed payment may create a late fee, a returned-payment fee, a failed-autopay fee, a cancellation notice, or a reinstatement charge if coverage stops and must be restored.

BNPL products are generally designed to split payments over time, and the CFPB has described BNPL as a form of credit that lets consumers split a purchase into smaller installments. Auto insurance billing is not always identical to retail BNPL, but the practical lesson is similar: read the payment terms before relying on the low first payment.[3]

- Ask when a payment is considered late.

- Ask whether there is any grace period.

- Ask whether failed autopay creates a separate returned-payment fee.

- Ask whether the insurer sends a cancellation notice after nonpayment.

- Ask how much must be paid to reinstate the policy after a lapse.

Cancellation and Reinstatement Fees

Cancellation and reinstatement are especially important because the cost is not only financial. If your auto insurance cancels for nonpayment, you may lose active coverage. Depending on your state, vehicle, and situation, that can create legal, lender, registration, or future insurance problems.

A reinstatement fee may apply when the provider allows a canceled policy to be restored. In some cases, the driver may need to pay the missed amount, a fee, and possibly a new down payment or rewritten policy amount. The exact process depends on the insurer, state, and timing of the cancellation.

| Scenario | Possible Cost | Why It Matters | Question to Ask |

|---|---|---|---|

| Late payment | Late fee or penalty | Raises the cost of that billing cycle. | How many days after the due date does the fee apply? |

| Returned payment | Bank-return, NSF, or failed-payment fee | A failed payment can create extra charges even if you try to pay again. | Can a declined card or failed bank draft trigger a fee? |

| Cancellation notice | Amount needed to keep coverage active | You may need to pay quickly to avoid a lapse. | How much time do I have before coverage stops? |

| Reinstatement | Missed payment plus possible reinstatement fee | Restoring coverage can cost more than simply staying current. | Is reinstatement guaranteed or subject to approval? |

| New policy after lapse | New first payment or higher quote | A lapse can make future shopping harder or more expensive. | Would a canceled policy require a new application? |

How to Calculate the Real Cost of BNPL Car Insurance Fees

The real cost is not only the amount due today. A better calculation includes the first payment, all scheduled installments, monthly service charges, payment processing fees, and any likely penalty charges. This helps you compare a low-upfront plan against a traditional installment plan or pay-in-full option.

1 Start with the full premium

Ask for the total premium over the full policy term. Do not compare one quote’s first payment against another quote’s full premium. Keep liability limits, deductibles, and optional coverages as similar as possible when comparing policies.

2 Add recurring billing charges

Add every installment, service, processing, or convenience fee that appears in the payment schedule. If a fee is charged every month, multiply it by the number of payments in the term.

3 Compare the full-term number

Compare the total paid by the end of the policy term. A BNPL-style option may still be worth it if cash flow is your main problem, but the decision should be based on the full cost, not only the startup amount.

Questions to Ask Before Enrolling

The NAIC’s consumer shopping materials encourage shoppers to compare policy details carefully and to compare similar coverage when reviewing auto insurance options. That same approach applies to BNPL-style fees: compare the payment terms, not only the advertised first payment.[4]

| Question | Why It Matters | Better Answer to Look For |

|---|---|---|

| What exactly is due today? | Some offers show a low first payment but add fees before activation. | A clear total that includes premium, taxes, fees, and payment-plan charges. |

| What fees apply every month? | Recurring charges can raise the full-term cost. | A complete schedule showing each payment and each fee. |

| Can I avoid fees by using autopay? | Some billing methods may cost less than others. | Clear explanation of whether autopay reduces, adds, or removes charges. |

| What happens if my payment fails? | A failed payment can cause fees and cancellation risk. | Written terms for returned payments, late fees, and cancellation notices. |

| What does reinstatement cost? | Restoring coverage after cancellation can be expensive or unavailable. | A clear reinstatement process before you enroll. |

| Would paying in full be cheaper? | Some installment fees may be avoided with full payment. | A side-by-side quote showing pay-in-full versus installment billing. |

When BNPL Car Insurance Fees May Still Be Worth It

Fees are not automatically a reason to reject a BNPL-style payment plan. For some drivers, a lower upfront amount can be useful if they need coverage quickly, are avoiding a lapse, or need to preserve cash for other urgent expenses. The key is knowing the cost before agreeing to the payment schedule.

Reasonable Use Cases

- You need proof of insurance quickly.

- You cannot comfortably pay a larger upfront amount.

- You understand the full payment schedule.

- The fees are clear and manageable.

- The coverage level still fits your needs.

Reasons to Be Careful

- The provider does not explain fees clearly.

- The monthly payment already feels too high.

- Late-payment rules are strict or unclear.

- Reinstatement terms are missing.

- The total cost is much higher than other quotes.

How This Page Differs From Hidden Fees

Expected fees and hidden fees are related, but they are not the same. This page explains the fee stages a driver should expect to ask about before choosing a pay-over-time plan. A hidden-fee issue is different: it usually involves charges that are unclear, poorly disclosed, easy to miss, or not explained until late in the quote or billing process.

That distinction matters for comparison shopping. A fee is not automatically unfair just because it exists. The bigger problem is when the fee is not clearly explained, not included in the full-term cost, or not visible until after the driver has already started the purchase process.

Related BNPLCI Guides

FAQ

What fees should I expect with BNPL car insurance?

You may see setup fees, application fees, installment fees, payment processing fees, late-payment fees, returned-payment fees, cancellation charges, or reinstatement costs. The exact fee structure depends on the insurer, provider, state, and payment plan.

Are BNPL car insurance fees the same as hidden fees?

No. This page focuses on fees you should expect and ask about before enrolling. Hidden fees are charges that may be unclear, poorly disclosed, or easy to miss during the quote or checkout process.

Can installment fees make car insurance more expensive?

Yes. A policy with a lower first payment can cost more overall if it includes recurring installment, service, processing, or convenience charges. Always compare the total paid over the full policy term.

What happens if I miss a BNPL car insurance payment?

A missed payment may trigger a late fee, returned-payment fee, cancellation notice, lapse, or reinstatement requirement. The exact consequences depend on the policy terms and state rules.

How can I reduce BNPL car insurance fees?

Ask for all fees in writing, choose a realistic payment schedule, keep payment information current, use autopay only if it fits your budget, and compare whether paying in full would reduce service charges.

Should I choose the plan with the lowest first payment?

Not automatically. The lowest first payment may not be the best value if the full-term cost, fees, coverage limits, deductibles, or cancellation rules are worse than another option.

Conclusion

BNPL car insurance fees can appear before coverage starts, during monthly billing, after a failed payment, or when a canceled policy must be reinstated. That is why the smartest comparison is not only the first payment. It is the full cost of the policy after every expected charge is included.

Before choosing a flexible payment plan, ask for the full premium, the amount due today, the complete payment schedule, all recurring fees, late-payment rules, failed-payment consequences, and reinstatement terms. A BNPL-style plan can be useful, but only when the fee structure is clear and the payment schedule is realistic.

References

- NAIC — Auto Insurance Shopping Tool and consumer guidance on comparing auto insurance coverage and cost. ↩

- New York Department of Financial Services — Insurance premiums and installment payment plan fee guidance. ↩

- Consumer Financial Protection Bureau — Buy Now, Pay Later market trends and consumer impacts. ↩

- NAIC — Tips for saving on auto insurance and comparing companies, coverage, service, dependability, and financial condition. ↩

Compare Auto Insurance Quotes by ZIP Code

Enter your ZIP code to compare auto insurance quote options and review coverage details before choosing a policy.

Compare price, coverage limits, deductibles, fees, payment terms, and policy conditions before choosing auto insurance.